Wealth Transfer Strategies for Asian HNWIs in 2026: Hong Kong & Singapore Lead the Greatest Intergenerational Shift in History

Discover why Hong Kong and Singapore are leading Asia’s great wealth transfer shift in 2026, and how HNWIs are planning legacy, liquidity, and succession with greater precision.

2nd Mar 2026 Insight

Wealth Transfer Strategies for Asian HNWIs in 2026: Hong Kong & Singapore Lead the Greatest Intergenerational Shift in History

People commonly ask:

Wealth transfer Asia Pacific 2026 forecast statistics

Hong Kong Singapore family office succession planning trends

HNWI life insurance estate planning Hong Kong 2026

Asia intergenerational wealth transfer USD 5.8 trillion

Trust structures vs life insurance wealth planning Singapore

What are the latest statistics on wealth transfer in Asia-Pacific for 2026-2030?

How do Hong Kong and Singapore family offices approach succession planning differently?

What percentage of Asian UHNW families have formal succession plans in 2026?

Which wealth transfer tools are most commonly used in Hong Kong vs Singapore?

What are the tax implications of cross-border wealth transfer for Asian HNWIs?

———————–

The Largest Wealth Transfer in Human History Is Happening Now in Asia

Between 2026 and 2030, an estimated USD 5.8 trillion will change hands across the Asia-Pacific region as the first generation of post-war wealth creators—entrepreneurs who built manufacturing empires, technology conglomerates, and regional trading networks—begin transferring their fortunes to the next generation. This isn’t merely a statistic. It represents the most consequential intergenerational wealth transition in human history, concentrated primarily across two financial hubs: Hong Kong and Singapore.

Yet despite the magnitude of this shift, 37% of Asian families currently lack formal succession plans, and among those who do have documentation, only 23% have translated these discussions into comprehensive, legally binding legacy frameworks. The result? A landscape where trillions in wealth are at risk of dissipation, family conflict, and value erosion within a single generation.

This article examines how Hong Kong and Singapore—Asia’s twin wealth management anchors—are addressing this challenge, the tools ultra-high-net-worth (UHNW) families are deploying, and the strategic frameworks that will define wealth preservation through 2030 and beyond.

Hong Kong vs Singapore: The Dual Engines of Asia’s Wealth Ecosystem

Hong Kong: The China Gateway with FIHV Tax Optimization

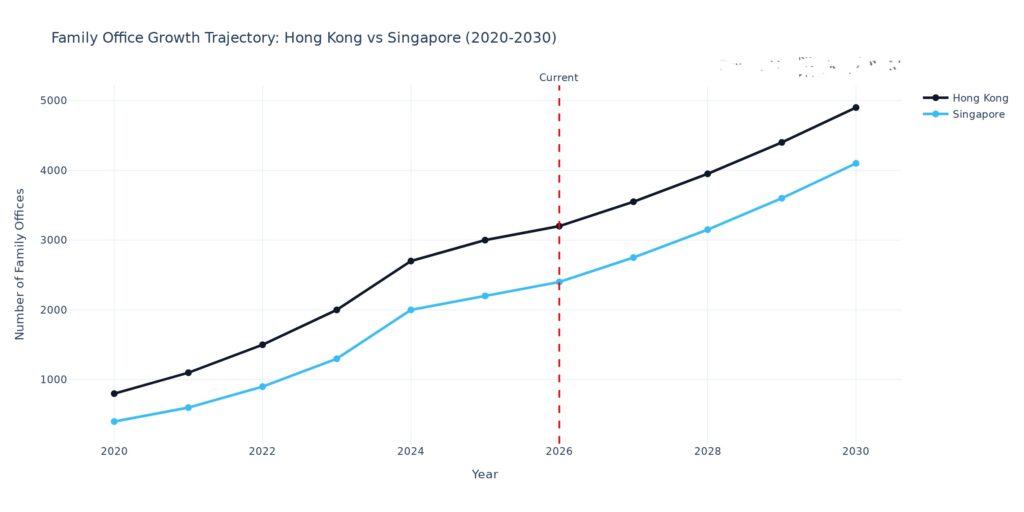

Hong Kong’s family office ecosystem has grown from approximately 800 offices in 2020 to over 3,200 by early 2026—a 300% increase in six years. The city’s appeal is threefold:

No capital gains tax, no withholding tax on dividends, no inheritance tax—creating tax-efficient structures for investment holding vehicles

Direct access to Mainland China markets—Hong Kong’s role as the gateway to the world’s second-largest economy remains unmatched

However, Hong Kong faces a critical succession planning gap. While 84% of Hong Kong HNWIs use life insurance as a wealth transfer tool (the highest rate in Asia), only 67% have formal succession plans in place. The disconnect reflects a cultural tendency to prioritize asset accumulation over governance frameworks—families focus on growing wealth but defer structuring its transition.

Singapore: The Stability Hub with Substance Requirements

Singapore’s family office population has surged from 400 in 2020 to 2,400 by 2026, with projections reaching 4,100 by 2030. The city-state’s competitive advantage centers on:

Regulatory predictability—Section 13O and 13U tax exemption schemes provide clarity, but require operational substance (local staff, defined economic activities)

Trust infrastructure maturity—Singapore’s trust adoption rate stands at 81%, the highest in Asia, supported by sophisticated trustee services and cross-border legal frameworks

Philanthropy Tax Incentive Scheme (PTIS)—encouraging single-family offices to establish Singapore as a regional philanthropy hub with 100% tax deductions on eligible overseas donations

Singapore’s strength lies in long-term wealth preservation and multi-generational governance. 78% of Singapore-based families have formal succession plans, and 61% report that the next generation is adequately prepared to inherit wealth—substantially higher than Hong Kong’s 48%.

The USD 5.8 Trillion Question: Where Is the Wealth Going?

Forecast: 2026-2030 Wealth Transfer Breakdown

Our analysis projects that:

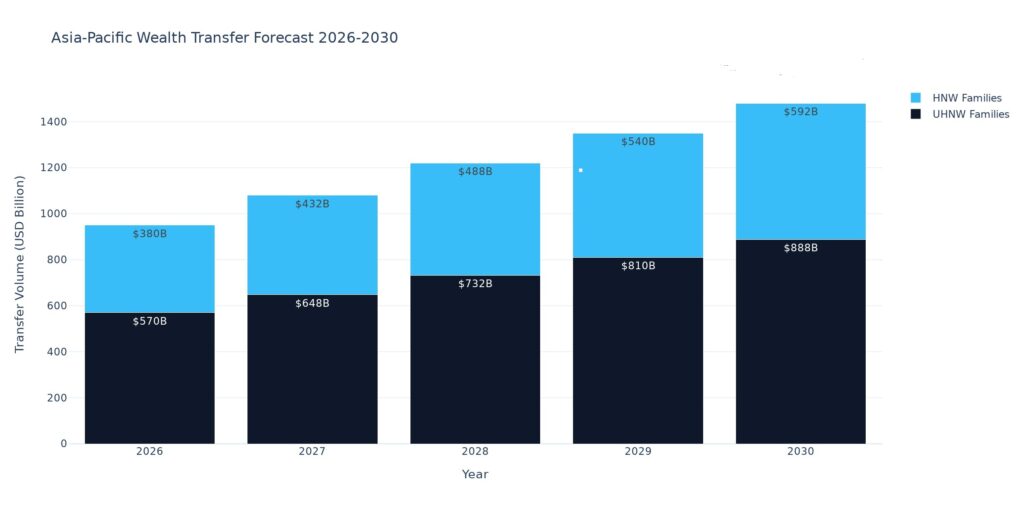

2026: USD 0.95 trillion will transfer, with USD 570 billion from UHNW families (assets >USD 30 million) and USD 380 billion from HNW families (USD 1-30 million)

2030: Annual transfer volume will reach USD 1.48 trillion, affecting an estimated 18,900 families across the region

Ultra-high-net-worth families will account for approximately 60% of total wealth transfer, making institutional-grade succession planning—family offices, trust structures, Jumbo life insurance—essential rather than optional.

A stacked bar chart titled “Asia-Pacific Wealth Transfer Forecast 2026-2030.” The chart projects the transfer volume in billions of USD from 2026 to 2030, broken down by UHNW Families (dark blue) and HNW Families (light blue). Total volumes show a steady year-over-year increase, starting at $950 billion in 2026 ($570B UHNW, $380B HNW) and reaching $1,480 billion by 2030 ($888B UHNW, $592B HNW).

The stacked bar chart illustrates the accelerating volume and composition of wealth transfers through 2030, with UHNW families (dark blue) dominating the transfer landscape.

The Succession Planning Preparedness Crisis

Why 70% of Family Wealth Disappears by the Second Generation

An oft-quoted study suggests that 70% of families see wealth dissipate by the second generation, and 90% by the third. While many Asian families defy this trend—particularly in Confucian-influenced markets where multi-generational legacy planning is culturally embedded—the data reveals systemic gaps:

Key findings:

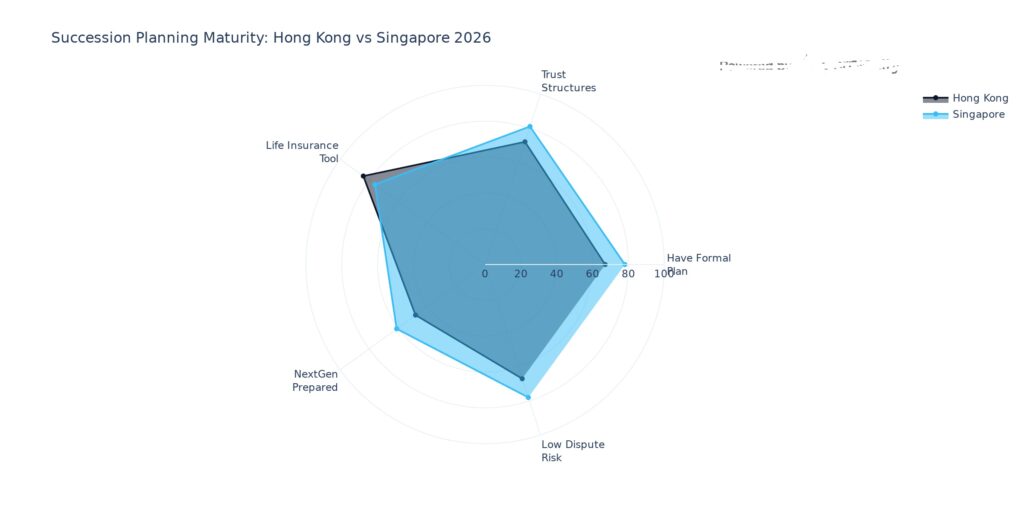

Japan leads in preparedness: 82% have formal plans, 72% report NextGen readiness, only 18% family dispute risk

Hong Kong middle-tier: 67% formal plans, but only 48% NextGen prepared, 33% dispute risk

Mainland China lags significantly: 54% formal plans, 37% NextGen prepared, 46% family dispute risk—the highest in Asia

India faces cultural challenges: Only 48% have formal plans, 52% dispute risk

Singapore stands out: 78% formal plans, 81% trust structure usage, 61% NextGen prepared, and only 22% family dispute risk—the lowest in the region.

The radar chart compares Hong Kong and Singapore across five critical dimensions, revealing Singapore’s structural advantage in trust infrastructure, NextGen preparation, and dispute prevention.

The Strategic Toolkit: How Asian HNWIs Are Structuring Wealth Transfer

1. Life Insurance: The Universal Foundation (76-84% Adoption)

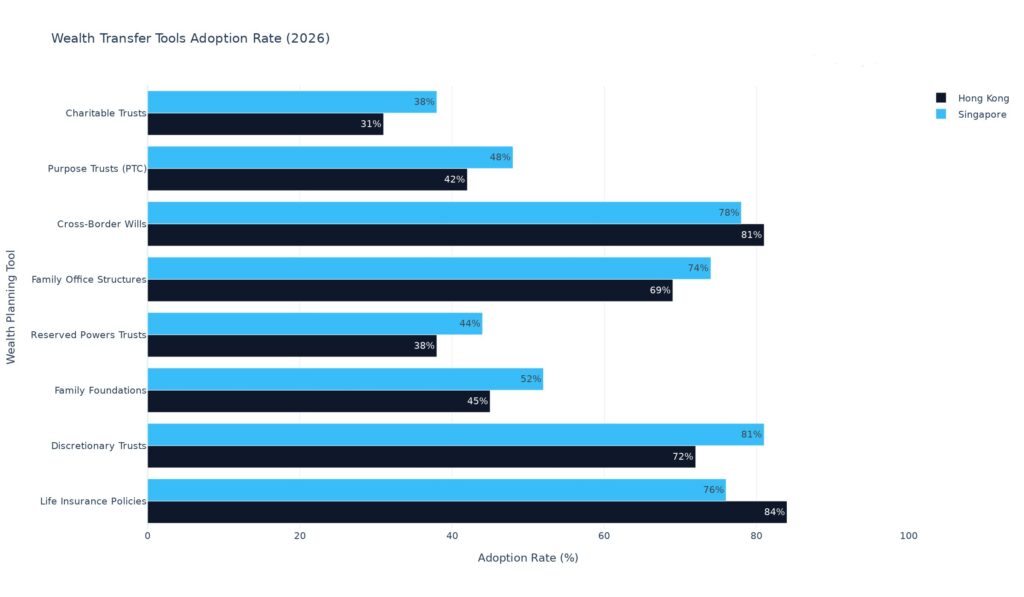

Life insurance remains the most widely adopted wealth transfer tool across Asia, with Hong Kong leading at 84% and Singapore at 76%. Why the dominance?

Advantages unique to Asia:

Bypasses probate processes—in jurisdictions like Hong Kong where estate settlement can be delayed for years due to legal disputes, life insurance pays directly to named beneficiaries, avoiding probate entirely

100% tax-free death benefit—in both Hong Kong and Singapore, life insurance proceeds are not subject to estate tax, inheritance tax, or income tax

Creditor protection—properly structured policies held within trusts or foundations provide institutional-grade asset protection

Flexible beneficiary designations—policyholders can specify exact payout percentages to multiple beneficiaries, preventing family disputes

Product evolution in 2026:

Hong Kong’s life insurance market recorded HK$264.5 billion (USD 34 billion) in new premiums from January-September 2025, a 56% year-over-year surge, driven substantially by mainland Chinese visitors and HNWIs seeking wealth transfer solutions. Products like Wealth Accelerator Whole Life Protection Plans now include:

Change of Life Insured option—enabling wealth transfer across generations until the original insured reaches age 130, with accumulated cash value continuing to grow

Policy Split Options—allowing policies to be divided among family members on a designated date or upon death, with flexible distribution percentages

Premium Prepayment Arrangements—providing upfront premium discounts of 5-13% for single-payment structures favored by UHNWIs

2. Discretionary Trusts: Singapore’s Structural Advantage (81% vs 72%)

Singapore’s 81% trust structure adoption reflects decades of legal infrastructure development, professional trustee services, and cross-jurisdictional frameworks. Trusts offer:

Legal separation of assets—removing wealth from personal estates, providing creditor protection and tax efficiency

Multi-generational governance—trustees manage distributions across generations per detailed, legally binding instructions (e.g., staggered payments at specific ages, conditional distributions tied to education milestones)

Reduced family conflict risk—professional trustees make decisions without emotional bias, preventing disputes that plague 33-52% of Asian families

Trust types gaining traction:

Discretionary (family) trusts (most common)—offering long-term flexibility as trustees adjust distributions to evolving family needs

Reserved powers trusts—allowing settlors to retain specific decision-making powers while benefiting from trust protections, appealing to Asian entrepreneurs accustomed to control

Non-charitable purpose trusts—used to hold shares in Private Trust Companies (PTCs), supporting business succession and governance continuity

Hong Kong’s 72% trust adoption trails Singapore but is growing rapidly, driven by FIHV structures that benefit from trust ownership for tax optimization.

3. Family Office Structures: The Institutional Framework (69-74%)

The line graph illustrates the exponential growth trajectory, with Hong Kong (dark blue) and Singapore (light blue) both projected to exceed 4,000 family offices each by 2030.

Family offices provide:

Centralized wealth governance—consolidating assets across jurisdictions under unified management

Professional succession planning—integrating legal, tax, investment, and governance expertise

Business succession support—managing ownership transitions in operating companies while preserving family control

Investment allocation priorities in 2026:

Private equity: 87% of Asian family offices invested, 18.1% average allocation, with plans to increase significantly

Real estate: Core holding for long-term stability and income generation

Alternative assets: Growing interest in venture capital, digital assets (subject to regulatory clarity)

ESG/impact investing: Increasing focus, particularly among NextGen heirs prioritizing social responsibility

4. Cross-Border Wills: The Overlooked Essential (78-81%)

Despite high adoption rates, cross-border wills remain underdisclosed. In Hong Kong, 28% of families keep wills undisclosed even to heirs, creating risks of:

Will validation disputes—lawsuits over estate distribution delaying wealth transfer

Conflicting jurisdictional claims—assets in multiple countries governed by different succession laws

Unintended disinheritance—outdated wills failing to reflect current family structures or asset locations

Best practice: Coordinate wills with trust structures and life insurance beneficiary designations to create a unified, conflict-free succession framework.

The NextGen Challenge: Are Heirs Ready to Inherit USD 5.8 Trillion?

The Preparedness Gap

Survey data reveals a troubling disconnect:

70% of families hold regular meetings to discuss wealth transfer

But only 30% have documented legacy plans

And just 23% have comprehensive succession frameworks

Among families that do have plans, 24% of parents believe their children are underprepared to inherit. The gap stems from:

Limited financial education—heirs report insufficient training in wealth management, investment strategy, and family governance

Lack of engagement—NextGen excluded from succession discussions until late in the process

Divergent priorities—younger generations prioritize entrepreneurship, social impact, and personal ventures over preserving family businesses

81% of NextGen HNWIs (aged 12-59) say they intend to switch their primary wealth management provider within two years of receiving inheritance, driven by dissatisfaction with:

Poor digital interfaces (generational technology expectations)

Limited access to alternative investments (private equity, venture capital, digital assets)

Lack of tailored, value-added services beyond traditional portfolio management

Strategic Recommendations: Building Anti-Fragile Wealth Structures

For Hong Kong-Based Families

Close the governance gap—formalize succession plans beyond asset accumulation; establish family councils, shareholder forums, and documented decision-making protocols

Leverage FIHV + trust combination—structure family office vehicles with trust ownership to optimize Hong Kong’s tax exemptions while embedding multi-generational governance

Prepare NextGen actively—integrate heirs into family office operations, provide formal financial education, and create mentorship frameworks

For Singapore-Based Families

Maximize trust infrastructure—Singapore’s 81% trust adoption reflects best practice; ensure Reserved Powers Trusts balance control with asset protection

Utilize PTIS for philanthropy—align wealth transfer with social impact through 100% tax-deductible overseas donations, creating legacy beyond financial capital

Adopt dual-hub strategies—anchor governance and preservation in Singapore while using Hong Kong for China market access and capital deployment

Universal Best Practices

Integrate life insurance as foundation—84% adoption in Hong Kong reflects proven effectiveness; ensure policies held in trusts/foundations with clear beneficiary structures

Address the 37% without plans—families without succession frameworks face 46-52% family dispute risk; formalize documentation immediately

Plan for 2030 acceleration—wealth transfer volume will increase 56% from 2026 to 2030; start structuring now to avoid forced decisions under pressure

Conclusion: From Intent to Action

Asia-Pacific stands at an inflection point. The USD 5.8 trillion wealth transfer through 2030 represents not just a generational shift, but a test of whether the region’s first-wave entrepreneurs can successfully institutionalize their legacies—or whether the “three-generation curse” will claim another cohort of fortunes.

Hong Kong and Singapore offer complementary strengths: Hong Kong excels in market access and tax efficiency; Singapore leads in governance maturity and trust infrastructure. The most sophisticated families are adopting dual-hub strategies, using both jurisdictions to optimize different aspects of wealth architecture.

But infrastructure alone isn’t enough. The 37% of families without formal plans, the 70% whose NextGen heirs feel unprepared, and the 46% facing family dispute risk must act decisively. Wealth transfer isn’t a transaction—it’s a multi-year process requiring legal frameworks, family governance, financial education, and cultural alignment.

The tools exist. The data is clear. The question now is execution.

The horizontal bar chart compares tool adoption rates between Hong Kong (dark blue) and Singapore (light blue), revealing strategic differences: Hong Kong leads in life insurance (84%), while Singapore dominates in trust structures (81%) and family foundations (52%).

General Counsel, Head of Compliance and Operations

Salah Mattoo is an experienced international lawyer and accomplished executive, currently serving as General Counsel and Head of Compliance. He specialises in dispute resolution, corporate and commercial transactions, regulatory compliance, and internal and external investigations across multiple jurisdictions.

Salah has acted in a range of high-profile international arbitration and cross-border litigation matters, representing corporate clients, sovereigns, and institutions in complex, high-stakes disputes. Salah's background includes advisory and leadership roles in sectors such as insurance, private equity, financial services, defence, commodities, energy, technology, and infrastructure.

In addition to his disputes practice, Salah has led the design and implementation of robust compliance programs aligned with international best practices, including AML, anti-bribery, sanctions, data privacy, ESG, and whistleblower frameworks. Salah regularly advises executive teams and boards on legal risk management, governance structures, and regulatory strategy.

With a strong track record in both contentious and transactional matters, Salah combines legal precision with strategic insight to support businesses navigating regulatory complexity and international growth. Salah is qualified in England & Wales, DIFC and ADGM. He has acted as lead counsel in international commercial courts, as well as in many international arbitrations seated in the leading arbitration centers, including Abu Dhabi, Dubai, Geneva, Hong Kong, London, New York, Paris, Riyadh, Singapore, Stockholm, Tokyo, Vienna, Washington and Zurich.

Salah holds a B.A. from University of California, Berkeley and an L.L.B and L.L.M. from The London School of Economics and Political Science (University of London).

Dubai · Geneva · Hong Kong · London · Singapore

Imran Khan

Founder & Managing Director

Imran Khan is a seasoned expert in private wealth planning and jumbo life insurance solutions, with over 10 years of experience advising ultra high net worth individuals (UHNWIs), families, and family offices across multiple jurisdictions. With a deep understanding of global wealth structuring, legacy planning, and asset protection, Imran is recognized for delivering highly customized strategies that align with clients personal, business, and multigenerational goals.

Throughout his career, Imran has worked closely with private banks, trust companies, and legal advisors to design and implement sophisticated structures involving international trusts, foundations, holding companies, and life insurance-based estate equalization plans. His expertise includes:

Life insurance for estate liquidity and succession planning

Cross-border wealth transfer and tax mitigation strategies

Pre-immigration and expatriation planning

Business continuity and key-person insurance for family enterprises

Family and corporate governance

Imran holds specialist accreditations in wealth planning and international insurance advisory and is a trusted advisor to clients across the Asia, Europe, Middle East and UK. Known for discretion, technical proficiency, and strategic insight, he has built enduring relationships with UHNW families seeking to preserve and grow their legacies in an increasingly complex regulatory environment.