Private Placement Life Insurance in Dubai: The Definitive Guide for High-Net-Worth Individuals (2026)

Executive Summary: Why Dubai HNWIs Are Choosing PPLI Over Traditional Wealth Planning Dubai has established itself as the global epicenter for ultra-high-net-worth individuals seeking sophisticated wealth preservation solutions. In 2025, the emirate boasts over 2,700 family offices and hosts a disproportionate concentration of global wealth—yet an alarming statistic persists: 76% of HNWIs lack comprehensive estate plans, leaving their […]

3rd Dec 2025 Blog

Private Placement Life Insurance in Dubai: The Definitive Guide for High-Net-Worth Individuals (2026)

Executive Summary: Why Dubai HNWIs Are Choosing PPLI Over Traditional Wealth Planning

Dubai has established itself as the global epicenter for ultra-high-net-worth individuals seeking sophisticated wealth preservation solutions. In 2025, the emirate boasts over 2,700 family offices and hosts a disproportionate concentration of global wealth—yet an alarming statistic persists: 76% of HNWIs lack comprehensive estate plans, leaving their legacies vulnerable to taxation, forced heirship rules, probate delays, and family disputes.

Enter Private Placement Life Insurance (PPLI): a sophisticated, tax-efficient wealth amplification tool increasingly favored by Dubai’s ultra-affluent. When combined with DIFC Foundations or ADGM Trusts, PPLI creates an integrated framework that simultaneously accomplishes wealth transfer, tax optimization, asset protection, and dynasty planning—objectives that traditional life insurance, wills, or standalone trusts cannot achieve independently.

This definitive guide explains PPLI mechanics in the Dubai context, contrasts it rigorously with traditional insurance, integrates it within DIFC Foundation and ADGM Trust frameworks, and provides actionable implementation checklists for HNWIs and their advisors.

1. What is PPLI and Why Dubai HNWIs Choose It

1.1 Demystifying Private Placement Life Insurance

Private Placement Life Insurance is a customized, non-standardized life insurance policy structured specifically to permit investment of policy premiums in a segregated, separately managed account (SMA) containing bespoke assets selected by the policyholder—not limited to the insurance company’s pre-approved investment menu.

Fundamentally, PPLI remains a qualifying life insurance product under IRC §7702 principles (recognized within US tax law and adopted by insurance regulators globally), meaning:

Investment gains within the policy accumulate tax-free (tax-deferred growth on capital gains, dividends, interest)

Death benefits pass to beneficiaries entirely income-tax-free (no ordinary income taxation)

The structure is compliant and IRS-recognized, supported by decades of private letter rulings to major families and institutions

The critical distinction from traditional VUL/IUL insurance: Rather than your premiums being invested in the insurance company’s approved mutual fund universe, your premiums fund a separately managed account with complete asset flexibility—hedge funds, private equity, real estate, private credit, crypto, structured products, or any permitted alternative investments.

Example: A Dubai entrepreneur worth USD 150M holds USD 35M in private equity fund interests generating 15% annual returns. Traditionally, this generates USD 5.25M in unrealized capital gains annually—taxable in their home jurisdiction (or potentially in UAE if deemed tax resident). Inside PPLI, the USD 35M compounds at 15% with zero annual tax liability, and upon the founder’s death, the accumulated USD 75M-100M+ transfers to beneficiaries entirely income-tax-free, with zero UAE probate when structured through a DIFC Foundation.

1.2 Why Dubai HNWIs Choose PPLI: Five Compelling Reasons

1: Regulatory Paradise for Wealth Structuring

Dubai offers the world’s most sophisticated, HNWI-friendly regulatory ecosystem:

DIFC Courts: Apply English common law (not UAE civil law), providing predictable, internationally recognized dispute resolution

DIFC Authority: Specialized financial services regulator with institutional expertise in complex structures

ADGM (Abu Dhabi Global Market): Parallel jurisdiction offering trusts, foundations, and family offices under common law principles

Zero Corporate Tax: No UAE corporate tax on DIFC-registered entities; no income tax on individuals (with limited exceptions)

No Estate Duty: Unlike most developed jurisdictions, Dubai/UAE impose no inheritance tax or estate duty

For HNWI families, this regulatory environment means: PPLI policies can be registered in DIFC/ADGM, held through DIFC Foundations or ADGM Trusts, and structured to pass to heirs with zero estate taxation, zero probate delay, and zero forced heirship complications.

2: Tax-Deferral Compounding for Alternative Asset Managers

HNWIs whose primary wealth originates from alternative investments (private equity, hedge funds, real estate development, venture capital) face extraordinary annual tax drag:

Hedge fund returns (short-term trading gains): Taxed as ordinary income (~37% marginal rate in many home jurisdictions)

Private equity distributions: Often taxed as ordinary income when exceeding long-term holding periods

Real estate appreciation: Subject to capital gains taxation upon sale

Private credit/lending: Interest income taxed annually

Inside PPLI: All of these returns compound tax-deferred. A USD 20M PPLI funded with PE/hedge fund interests, generating 12% annual returns, produces:

Year 10 cumulative: USD 62.1M value (taxable elsewhere: USD 8.9M total taxes paid; PPLI: USD 0 total taxes)

Upon death: USD 62.1M passes to heirs income-tax-free (taxable elsewhere: heirs owe any estate taxes)

This compounding differential creates USD 8M-15M in lifetime wealth preservation for moderate UHNWI families—justifying the PPLI infrastructure.

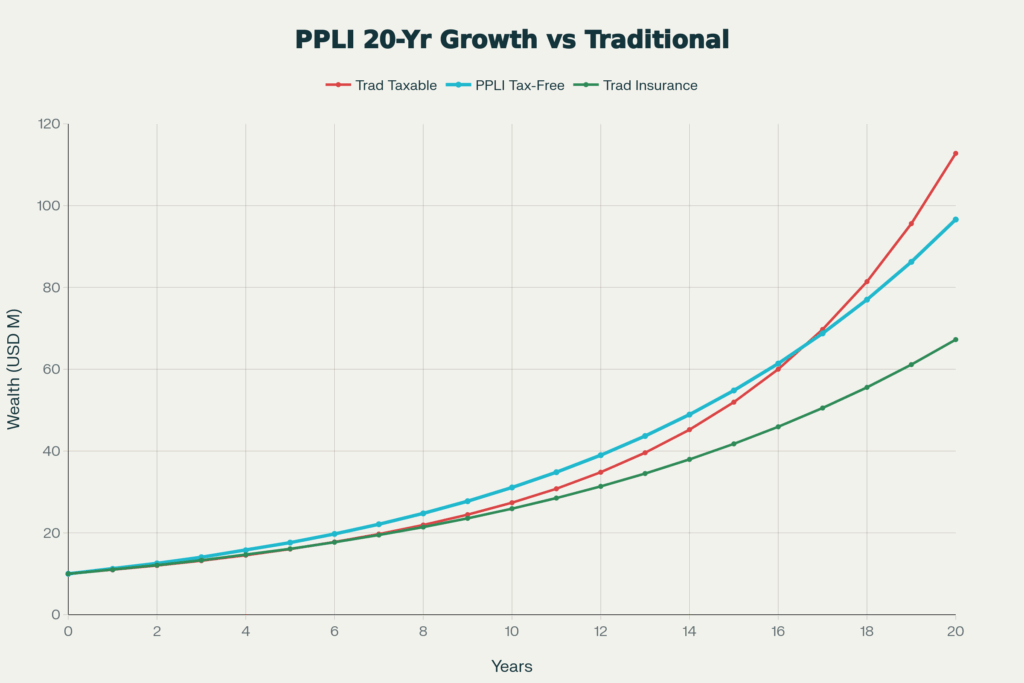

20-year wealth accumulation projection illustrating PPLI’s tax-deferred compounding advantage. Despite identical 12% gross investment returns, PPLI significantly outpaces both taxable and traditional insurance vehicles, generating USD 96.6M vs USD 112.8M (taxable pays embedded taxes) vs USD 67.3M (traditional insurance with limited returns)

3: Alternative Asset Deployment Without Liquidity Sacrifice

Many Dubai HNWIs hold substantial illiquid positions: private company shares, real estate, private equity fund interests, venture capital stakes. These cannot be easily sold, pledged, or repositioned without triggering taxation or legal complications.

PPLI permits housing these illiquid assets within the insurance wrapper, thereby:

Locking in tax-deferred treatment without forcing liquidation

Enabling Lombard loans (collateral-backed borrowing) against the policy value for current liquidity needs

Preserving upside while accessing capital for expansion, acquisitions, or lifestyle purposes

Structuring multi-generational transfer without forced sale

Example: Dubai real estate developer holds USD 40M in completed properties. Rather than selling (triggering capital gains tax), properties can be placed in PPLI through real estate fund structures, generating tax-deferred growth + providing collateral for Lombard lending without liquidation.

4: Asset Protection from Personal Liabilities and Forced Heirship

A profound advantage in Middle East planning: protection from forced heirship laws.

Under UAE/Islamic inheritance law, when a Muslim individual dies, their estate is typically divided per Islamic succession rules (spouse receives 1/4-1/2; children receive remainder; siblings/parents may claim portions). These rules cannot be altered by will and supersede contractual intentions.

However: Assets held in a DIFC Foundation or ADGM Trust—not in the individual’s personal name—bypass forced heirship rules entirely. And when PPLI is owned by such structures:

Policy proceeds remain outside the deceased’s personal estate (not subject to Islamic succession)

Death benefit passes directly to beneficiaries per trust/foundation design, not per Islamic law

Family succession intentions are honored exactly as structured

For non-Muslim expatriates, PPLI held in DIFC/ADGM structures similarly protects against:

Creditor claims from business liabilities

Divorce settlements (assets in trust/foundation often protected)

Forced heirship complications if tax residence changes

Regulatory seizure or sanctions risk (segregated SMA provides some insulation)

5: Cross-Border Mobility and Global Family Planning

Dubai’s HNWIs increasingly span multiple jurisdictions: homes in Dubai, London, New York, and Singapore; business interests in Greater China, Europe, and Southeast Asia; family members scattered globally.

PPLI registered in DIFC or ADGM (with English common law governance) is recognized in major financial centers—far more portable and internationally understood than UAE-specific structures. When combined with ADGM Trusts (which follow English trust law) or DIFC Foundations (hybrid common/civil law), the structure facilitates:

Cross-border beneficiary designations without conflict-of-law complications

Seamless integration with family office operations in Singapore, London, or New York

Succession planning that adapts as family circumstances evolve across jurisdictions

2. PPLI vs Traditional Life Insurance in the UAE Context

2.1 Feature-by-Feature Comparison

The following comparison demonstrates why PPLI, while substantially more complex and costly than traditional insurance, provides transformational value for UHNWI segments:

Key Differentiation Points:

Feature

PPLI Advantage

Traditional Insurance Advantage

Investment Universe

Unlimited alternatives (PE, hedge funds, real estate, private credit, crypto)

Constrained to insurer-approved products (mutual funds, indices, sub-accounts)

Portfolio Control

Independent manager maintains investment discretion; aligns with family strategy

Insurer maintains control; limited customization

Cost of Insurance (COI)

Lower (0.5-1.0% of NAR); compensated by superior investment returns

Higher (1.0-2.5% of NAR); built into policy pricing

Tax Efficiency

Exceptional for high-tax-bracket investors; eliminates annual capital gains taxation

Beneficial at all tax brackets; standard insurance treatment

Probate Bypass

Eliminated through trust/foundation ownership; complete avoidance

Partially achieved; depends on beneficiary designation precision

20-year accumulation: USD 47M (superior to taxable due to compounding, inferior investment returns)

Scenario C: PPLI with 15% Alternative Asset Strategy

Annual return: USD 7.5M

Tax within policy: USD 0 (deferred entirely)

After-tax return: USD 7.5M (full 15%)

20-year accumulation: USD 96.6M

Wealth Transfer Differential: USD 96.6M (PPLI) vs USD 62M (taxable) = USD 34.6M additional wealth (55% greater accumulation)

Upon death, the PPLI proceeds transfer to heirs income-tax-free and—if structured in DIFC Foundation—estate-tax-free. Traditional taxable account heirs receive only USD 62M after embedded taxes.

3. PPLI Within DIFC Foundations: Creating a Perpetual Wealth Dynasty

3.1 Understanding DIFC Foundations

The Dubai International Financial Centre (DIFC) Foundation is a legal vehicle governed by the DIFC Foundations Law 2007, recognized under English common law principles. Key characteristics:

Entity Structure:

Independent legal personality (separate from founder)

No shareholders; instead governed by a Foundation Council

Founder establishes a Charter defining governance, purposes, and succession

Council Members appointed (and replaced) per Charter provisions

Guardian role optional; can be appointed to oversee Council decisions

Perpetual Duration:

Unlike trusts (which terminate after specified periods), DIFC Foundations can exist indefinitely

Assets remain within Foundation structure across generations without transfer/probate

Founder’s governance intentions embedded in Charter; survive founder’s death

Asset Holding:

Foundation directly owns assets (registered in Foundation name)

Founder transfers assets to Foundation (irrevocable)

No transfer of ownership at death (Foundation continues; beneficiaries receive distributions per Charter)

3.2 DIFC Foundation + PPLI Integration: The Perpetual Wealth Structure

Optimal Architecture:

Component

Details

FOUNDER

• Creates and signs the DIFC Foundation Charter• Defines succession terms and beneficiary distribution rules

DIFC FOUNDATION (Legal Entity)

• Holds assets on behalf of Founder• Operates according to the Charter

PPLI Policy (Owned by Foundation; Founder = Insured)

• Annual Premium: USD 3M–5M • Investment Structure: Segregated Managed Account (SMA) with PE, hedge funds, real estate • Death Benefit: USD 20M–50M (insurance leverage) • Tax Treatment: 0% tax on growth inside the policy (deferral) • On Founder’s Death: USD 20M–50M is paid directly to the Foundation for distribution as per Charter

Real Estate Assets (Held by Foundation)

• Dubai property • UAE real estate holdings • Legally registered in Foundation’s name

Investment Portfolio (Held by Foundation)

• Public market investments (stocks, bonds) • Fund interests and alternative investments

BENEFICIARY STRUCTURE (Specified in Charter)

• Spouse: Lifetime annuity or percentage-based distributions • Children: Age-gated distributions (e.g., at 21, 30, 40) • Grandchildren: Lifetime beneficial interests • Charitable Allocations: Optional—can function as a perpetual philanthropy vehicle

3.3 DIFC Foundation + PPLI Benefits: The Five-Layer Advantage

Layer 1: Tax Efficiency

DIFC Foundation: 0% corporate tax; 0% income tax on distributions

PPLI: 0% tax on internal growth; tax-free death benefit

Combined Effect: Extraordinary compounding with zero annual tax friction

Layer 2: Perpetual Continuity

DIFC Foundation never terminates (unlike trusts with vesting or termination dates)

Result: Maximum wealth preservation against litigation, regulatory action, or family disputes

4. PPLI Within ADGM Trusts: Global Flexibility and Common Law Recognition

4.1 Understanding ADGM Trusts

The Abu Dhabi Global Market (ADGM) Trust operates under the Trusts (Special Provisions) Regulations 2016, following English common law trust principles. Key distinctions from DIFC Foundations:

Trust Structure:

Settlor (asset owner) transfers legal title to Independent Trustee

Separation of legal title (Trustee) and beneficial interest (Beneficiaries)

Trustee holds assets for beneficiaries’ benefit per Trust Deed

No separate legal entity; Trust is contractual relationship

Flexibility Advantages:

Trustee succession can be modified per Trust Deed

Beneficiary interests can be defined with granularity (income, capital, discretionary)

Trust can terminate at specified time (unlike perpetual Foundations)

Protector role common; provides beneficiary oversight of trustee

Portability:

Trust Deed governed by ADGM law; assets can be physically located anywhere (Dubai, Singapore, US, etc.)

Greater flexibility for internationally mobile families

English common law recognized globally

4.2 ADGM Trust + PPLI: The Flexible Global Architecture

4.3 ADGM Trust + PPLI Advantages: Global Sophistication

Advantage #1: Trustee Succession Clarity

Unlike Foundations requiring Council changes, Trusts name successor trustees directly in deed

Clear chain of succession eliminates governance vacuum

Successor trustee authority automatic upon predecessor death/removal

Advantage #2: Beneficiary Customization

Trust Deed permits precise distribution rules: income to spouse during life, capital to children post-spouse death

Discretionary standards can condition distributions on beneficiary circumstances

Spendthrift provisions protect beneficiaries from creditors

Example: “Trustee shall distribute income to Spouse for life; upon Spouse’s death, Trustee shall distribute capital to Children in equal shares, provided that distributions conditioned on each Child reaching age 25 and completing higher education”

Advantage #3: International Portability

ADGM Trust can hold assets in multiple jurisdictions without conflict-of-law issues

PPLI registered in DIFC or ADGM can be owned by ADGM Trust without complication

If Settlor relocates, Trust governance automatically follows (no re-registration required)

Advantage #4: Protector Oversight

Optional Protector role (separate from Trustee) provides beneficiary advocacy

Protector can: (a) approve material trustee decisions, (b) remove trustee for cause, (c) modify trust terms in limited scenarios

Balances trustee power with family protection

5. DIFC Foundation vs ADGM Trust: Which Structure for Your PPLI?

5.1 Decision Framework

Family Characteristic

DIFC Foundation Better

ADGM Trust Better

Primary Objective

Perpetual dynasty (indefinite wealth transfer across infinite generations)

Multi-generational flexibility (typically 3-4 generations, then evaluation)

Wealth Profile

Very large assets (USD 50M+); seeking perpetual compounding

DIFC Foundation + PPLI: Optimal for Dubai-centric UHNWIs with USD 50M+ net worth, clear founder governance preferences, and perpetual dynasty ambitions.

ADGM Trust + PPLI: Superior for globally mobile UHNWI families, multi-jurisdictional assets, and flexibility concerns.

Dual Structure (DIFC Foundation + ADGM Trust + PPLI): For ultra-sophisticated families with USD 100M+ net worth wanting: (a) DIFC Foundation holds UAE real estate/primary assets; (b) ADGM Trust holds liquid investments/international assets; (c) PPLI owned by both through specialized sub-structure. Most complex; requires institutional-level governance.

6. How PPLI Protects High-Net-Worth Assets: Asset Protection Mechanics

6.1 Segregation of Assets: The Multi-Layer Architecture

PPLI provides asset protection through three distinct segregation layers:

Layer 1: Separate Account Segregation (SMA)

Insurance company (policy custodian) holds PPLI assets in segregated account (not in general account with other policyholders)

Legal title held by insurance company; beneficial interest belongs to policyholder/trust

If insurance company fails: SMA assets transfer to assumption company or successor insurer; unaffected by general account creditors

Layer 2: Policy-Level Creditor Protection

Insurance regulation in DIFC/ADGM (following English law) provides creditor protection: policy assets cannot be attached by policyholder’s creditors (with limited exceptions)

Creditor cannot force surrender/liquidation of policy to satisfy judgment

Foundation Council/Trustee provides annual statements to beneficiaries

Periodic family meetings review strategy + address questions

3-5 year comprehensive review (market changes, family circumstances, law changes)

Outcome: Compliant, governed structure with clear stakeholder communication

8. Cost-Benefit Analysis: Is PPLI Right for Your Situation?

8.1 Total Cost of Ownership Model

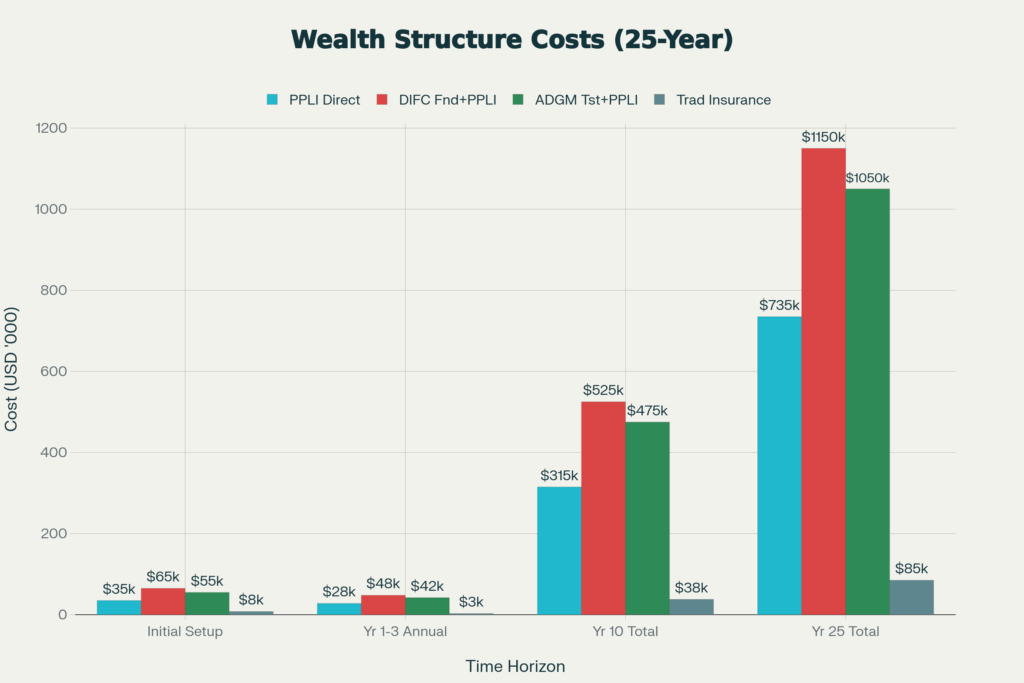

Comparative cost analysis of four wealth planning vehicles over 25-year lifecycle. While upfront costs are higher for PPLI + Foundation/Trust structures, tax savings and asset protection benefits justify investment for UHNWI segment (USD 25M+ net worth)

PPLI Costs (Annual Basis):

Cost Category

Range (Annual)

Example (USD 5M Premium)

Policy Mortality & Expense (M&E)

0.5-1.0% of policy value

USD 25,000-50,000

Cost of Insurance (COI)

0.5-1.0% of death benefit NAR

USD 50,000-100,000

Policy Administration Fee

Flat or % of cash value

USD 5,000-15,000

Investment Manager Fee

0.25-0.75% of SMA assets

USD 12,500-37,500

Trustee/Foundation Admin

Annual compliance + governance

USD 10,000-25,000

Annual Tax/Compliance

Accounting + legal review

USD 5,000-15,000

Insurance Broker Fee

Typically inside policy cost

USD 0-5,000

TOTAL ANNUAL COST

Range

USD 107,500-242,500

8.2 Breakeven Analysis

Question: When does the tax-deferral benefit justify PPLI costs?

Assumptions:

Client net worth: USD 50M

Alternative asset holdings: USD 20M (in PPLI)

Annual gross return: 12%

Annual return = USD 2.4M

Annual tax (outside PPLI, ordinary income rate): USD 888K (37%)

Long-term ROI: USD 14.76M net benefit over 20 years (988% ROI on total PPLI costs)

8.3 When PPLI is NOT Justified

PPLI is economically unjustifiable if:

Net Worth < USD 10M: PPLI costs disproportionate to tax savings

Low-Tax-Drag Assets: Municipal bonds, tax-loss harvested portfolios, or tax-efficient ETFs already minimize taxation

Short Time Horizon: Less than 5-year planning window reduces compounding benefit

Liquid, Easily-Managed Assets: Public securities requiring rebalancing may violate investment control doctrine

Conservative Return Expectations: Expected returns < 8% annually may not justify fees

9. Common PPLI Misconceptions Debunked

Misconception #1: “PPLI is a Tax Shelter Subject to IRS Crackdown”

Reality: PPLI is a legitimate, IRS-approved strategy supported by:

Explicit IRC §7702 and §817(h) statutory framework

Decades of Private Letter Rulings issued to major families and institutions

Major insurance carriers offering PPLI products without regulatory concern

DIFC/ADGM regulatory recognition

Fact Check: The IRS has never disallowed a properly-structured PPLI policy where §7702 and §817(h) requirements are satisfied. Tax shelters—structures designed primarily to avoid taxes rather than serve genuine insurance purposes—are scrutinized. PPLI serves legitimate succession planning + wealth transfer purposes alongside tax efficiency; therefore it remains compliant.

Truth: Over-aggressive PPLI structures claiming tax deductions or improper basis treatment face challenges. Compliant PPLI structures—with independent investment managers and proper diversification—are universally accepted.

Misconception #2: “PPLI is Only for Billionaires”

Reality: PPLI is accessible to USD 20M-30M+ net worth individuals. While startup costs are substantial (USD 30K-50K), ongoing costs (USD 100K-200K annually) represent 0.3-1% of net worth—economically justified for larger HNWIs.

Fact Check: A USD 25M HNWI with USD 10M in alternative assets generating 12% returns pays approximately USD 150K annually in PPLI costs but saves USD 400K+ in annual taxes—net benefit of USD 250K+.

Truth: PPLI is economically justified for HNWIs with USD 25M+ net worth + alternative asset holdings. Below USD 25M, traditional insurance may suffice.

Misconception #3: “PPLI is Too Complex to Manage”

Reality: Post-implementation, PPLI requires minimal active management:

Complexity is primarily front-loaded: Initial setup requires legal/insurance/investment team coordination. Once operational, PPLI governance is straightforward institutional-level administration.

Truth: A professional family office or institutional trustee manages PPLI governance seamlessly, similar to trust administration. Complexity is overhead, not operational burden.

Misconception #4: “DIFC Foundations and ADGM Trusts are Unrecognized Outside UAE”

Reality: Both structures enjoy substantial international recognition:

English common law principles internationally understood

DIFC Courts award precedent; ADGM structures recognized by major financial institutions

Banks in Singapore, London, New York, Hong Kong honor DIFC/ADGM trust deeds + foundation charters

Tax treaties between UAE and major jurisdictions recognize trust/foundation status

Fact Check: Global financial institutions increasingly service DIFC/ADGM structures for UHNWI clients. Recognition has grown substantially since 2015+.

Truth: DIFC and ADGM provide the most internationally portable wealth structures available in the Middle East, comparable to Singapore, Luxembourg, or English trusts.

Misconception #5: “PPLI Cannot Hold Illiquid Assets”

Reality: PPLI can hold any permitted asset, including:

Private equity fund interests

Illiquid real estate positions

Operating business shares

Private credit holdings

Cryptocurrency wallets

Intellectual property interests

Mechanism: Assets transfer to SMA; independent manager holds assets per investment mandate. Illiquidity is not an obstacle—indeed, illiquid alternative assets are PPLI’s primary use case.

Fact Check: Successful PPLI policies routinely house founder private equity stakes, real estate, and venture holdings without issue.

Truth: PPLI is ideal for illiquid asset holders seeking tax-deferred compounding without forced liquidation.

10. PPLI Implementation Checklist for Wealth Advisors

Critical Questions Before Recommending PPLI

□ Client Suitability Assessment

Verify net worth (USD 25M+ recommended; minimum USD 10M if exceptional circumstances)

Assess alternative asset holdings (USD 5M+ in illiquid positions ideal)

Has client decided between: (a) DIFC Foundation, (b) ADGM Trust, or (c) dual structure?

Does structure align with regulatory residency and jurisdiction?

Is trustee/council governance acceptable to client?

Has cross-border tax impact been modeled?

□ Tax and Legal Compliance

Has client’s tax advisor confirmed home jurisdiction tax implications?

Have CRS/FATCA reporting requirements been addressed?

Is DIFC Foundation/ADGM Trust registered with authorities?

Has legal documentation (Charter/Trust Deed) been executed and registered?

□ Investment and PPLI Specifics

Has independent investment manager been selected and approved?

Is manager experienced with §817(h)-equivalent diversification requirements?

Have target SMA assets been identified and approved?

Has insurance carrier completed preliminary underwriting?

Are expected returns (8-12%+) sufficient to justify PPLI costs?

□ Governance and Administration

Are Foundation Council Members or Trust Trustees identified and appointed?

Has annual compliance process been defined (meetings, reporting, reviews)?

Are beneficiary communication protocols established?

Has 3-5 year review schedule been calendared?

□ Costs and Economics

Have all costs been itemized and disclosed to client (setup + annual)?

Has breakeven analysis demonstrated ROI?

Are costs acceptable relative to net worth and tax savings?

Has insurance financing option been evaluated (if applicable)?

□ Documentation and Records

Is all correspondence with insurance company documented?

Are investment manager agreements archived?

Is DIFC/ADGM registration documentation filed?

Are beneficiary notifications documented?

11. Closing: PPLI as the Cornerstone of Dubai-Based Dynasty Planning

The extraordinary wealth concentration in Dubai—combined with the UAE’s unique regulatory environment, zero-tax framework, and English common law courts—creates an unparalleled opportunity for UHNWI families to preserve, amplify, and transfer generational wealth with minimal friction.

Private Placement Life Insurance, when integrated with DIFC Foundations or ADGM Trusts, transforms insurance from a passive protection tool into an active wealth amplification engine. By enabling tax-deferred compounding of alternative assets, providing death benefit leverage for succession liquidity, offering multi-layer asset protection, and creating perpetual family governance structures, PPLI addresses the precise objectives that characterize advanced UHNWI planning:

Tax Efficiency: Zero annual taxation on investment returns (vs. 37%+ external taxation)

Wealth Amplification: Achieving 12%+ returns with tax-deferral vs. 8%+ after-tax returns

Succession Certainty: Guaranteed death benefit providing immediate liquidity for family/business continuity

Generational Continuity: Perpetual Foundation structure enabling infinite-timeline wealth compounding

For the estimated USD 5.8 trillion in intergenerational wealth transfer occurring in Asia by 2030, bespoke structures combining PPLI + DIFC Foundations + ADGM Trusts represent the state-of-the-art planning architecture. Dubai-based HNWIs who deploy these structures now—before regulatory changes, tax law updates, or family disputes—position themselves and their families for multi-generational prosperity.

The window of opportunity is now. Connect with Sphere Private’s PPLI specialists to explore your customized wealth structuring strategy.

General Counsel, Head of Compliance and Operations

Salah Mattoo is an experienced international lawyer and accomplished executive, currently serving as General Counsel and Head of Compliance. He specialises in dispute resolution, corporate and commercial transactions, regulatory compliance, and internal and external investigations across multiple jurisdictions.

Salah has acted in a range of high-profile international arbitration and cross-border litigation matters, representing corporate clients, sovereigns, and institutions in complex, high-stakes disputes. Salah's background includes advisory and leadership roles in sectors such as insurance, private equity, financial services, defence, commodities, energy, technology, and infrastructure.

In addition to his disputes practice, Salah has led the design and implementation of robust compliance programs aligned with international best practices, including AML, anti-bribery, sanctions, data privacy, ESG, and whistleblower frameworks. Salah regularly advises executive teams and boards on legal risk management, governance structures, and regulatory strategy.

With a strong track record in both contentious and transactional matters, Salah combines legal precision with strategic insight to support businesses navigating regulatory complexity and international growth. Salah is qualified in England & Wales, DIFC and ADGM. He has acted as lead counsel in international commercial courts, as well as in many international arbitrations seated in the leading arbitration centers, including Abu Dhabi, Dubai, Geneva, Hong Kong, London, New York, Paris, Riyadh, Singapore, Stockholm, Tokyo, Vienna, Washington and Zurich.

Salah holds a B.A. from University of California, Berkeley and an L.L.B and L.L.M. from The London School of Economics and Political Science (University of London).

Dubai · Geneva · Hong Kong · London · Singapore

Imran Khan

Founder & Managing Director

Imran Khan is a seasoned expert in private wealth planning and jumbo life insurance solutions, with over 10 years of experience advising ultra high net worth individuals (UHNWIs), families, and family offices across multiple jurisdictions. With a deep understanding of global wealth structuring, legacy planning, and asset protection, Imran is recognized for delivering highly customized strategies that align with clients personal, business, and multigenerational goals.

Throughout his career, Imran has worked closely with private banks, trust companies, and legal advisors to design and implement sophisticated structures involving international trusts, foundations, holding companies, and life insurance-based estate equalization plans. His expertise includes:

Life insurance for estate liquidity and succession planning

Cross-border wealth transfer and tax mitigation strategies

Pre-immigration and expatriation planning

Business continuity and key-person insurance for family enterprises

Family and corporate governance

Imran holds specialist accreditations in wealth planning and international insurance advisory and is a trusted advisor to clients across the Asia, Europe, Middle East and UK. Known for discretion, technical proficiency, and strategic insight, he has built enduring relationships with UHNW families seeking to preserve and grow their legacies in an increasingly complex regulatory environment.