What the Indexed Universal Life 2025 Regulatory Shift Means for Professional Investors in Hong Kong

The March Circular That Changed the Game On March 13, 2025, the Hong Kong Insurance Authority (IA) and Hong Kong Monetary Authority (HKMA) issued a joint circular that quietly opened a door many thought would stay shut. For the first time, Indexed Universal Life Insurance (IUL)—a sophisticated wealth-management product long restricted by regulatory concerns—became available […]

5th Jan 2026 Life Insurance

What the Indexed Universal Life 2025 Regulatory Shift Means for Professional Investors in Hong Kong

The March Circular That Changed the Game

On March 13, 2025, the Hong Kong Insurance Authority (IA) and Hong Kong Monetary Authority (HKMA) issued a joint circular that quietly opened a door many thought would stay shut. For the first time, Indexed Universal Life Insurance (IUL)—a sophisticated wealth-management product long restricted by regulatory concerns—became available to Hong Kong’s professional investor segment.[1]

This wasn’t a sweeping retail rollout. Instead, it was a surgical regulatory adjustment: IUL products targeting high-net-worth individuals (HNWIs) who meet the definition of “professional investors” under the Securities and Futures Ordinance could now be offered with streamlined approval procedures, relaxed suitability requirements, and exemptions from certain retail-protection rules that had historically blocked these products.[2][3]

For wealth-planning advisors in Hong Kong, this development matters. It represents the regulator’s confidence that sophisticated investors can handle IUL’s complexity without the extensive handholding required for retail customers. For HNWIs, it opens access to a product class that combines lifetime insurance protection with market-linked growth—something traditional whole-life policies cannot offer.

Understanding IUL: The Mechanics

Before examining the regulatory shift, it’s worth clarifying what IUL actually is.

Traditional universal life insurance gives you:

Lifetime death benefit (as long as premiums are paid)

A cash-value component that earns a fixed or floating interest rate set by the insurer

Flexibility to adjust premiums and death benefits as circumstances change

Tax-deferred growth on the cash value

Indexed universal life keeps all of this, but with one critical difference: instead of a fixed interest rate, your cash value grows (or shrinks) based on the performance of a financial index—typically a stock-market index like the S&P 500 or the Hang Seng.[4]

The mechanics work like this: If the S&P 500 rises 15% in a given year, your policy’s cash value might earn 12% (the insurer typically applies a “cap” to limit their exposure). If the market falls 10%, you earn 0% that year (the “floor” protects you from losses).[5]

This differs fundamentally from traditional vehicles:

Investment-linked assurance schemes (ILAS): Direct exposure to mutual funds held inside the policy. Higher volatility, stricter regulations.

IUL offers middle ground: market participation with downside protection, packaged inside a permanent insurance wrapper—a critical distinction for HNWIs managing substantial multi-jurisdictional wealth.

The 2025 Regulatory Landscape: Class C Business Classification

The March 2025 circular classified IUL as “Class C (linked long-term) business” under Hong Kong’s Insurance Ordinance.[1]

This classification matters because:

1. Clear Regulatory Framework Rather than leaving IUL in legal limbo, the IA explicitly stated which guidelines apply: GL15 (Underwriting Class C Business), GL26 (Sale of ILAS Products), GL28 (Benefit Illustrations), and GL30 (Financial Needs Analysis).[1]

2. Flexibility for Professional Investors The circular noted that “certain provisions are not strictly relevant” to IUL and can be modified when products are sold exclusively to professional investors. This reduces onerous suitability requirements without compromising consumer protection.[2]

3. Retail Exclusion as Safeguard IUL products marketed into Hong Kong must be reserved for clients meeting the SFO definition of professional investors—HNWIs with substantial investment experience and financial resources.[3][1]

In practical terms: if you’re a professional investor in Hong Kong seeking IUL, the insurer must still demonstrate suitability. But they don’t need to conduct the exhaustive financial-needs analysis required for retail customers buying ILAS or whole life.

This regulatory balance—clear guardrails for consumer protection with flexibility for sophisticated buyers—explains the circular’s positive reception and its role in enabling responsible innovation.[6][2]

Product

Annual Cap(%)

Floor Protec. (%)

Entry Fee (%)

Admin Fee ($/mo)

Sun Life IUL

12%

0%

7.5%

$10.00

HSBC Aspire

14%

0%

6.0%

$15.00

YF Life IUL

13%

0%

4.5%

$7.50

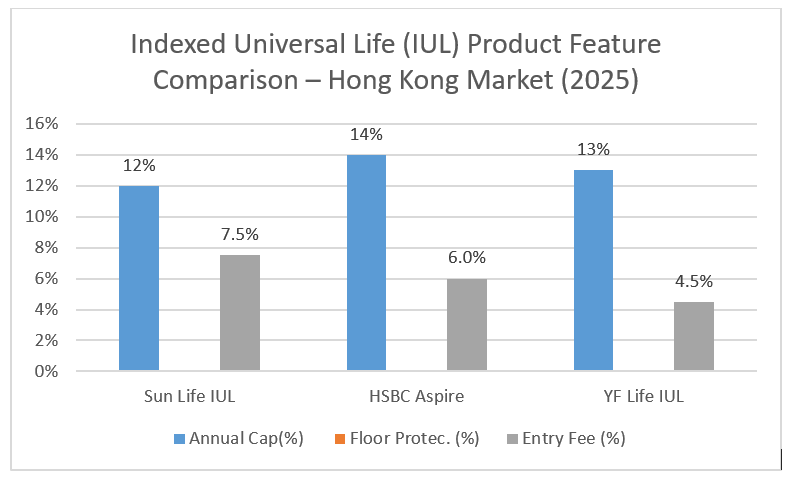

Hong Kong’s three early-mover IUL products (May-July 2025 launches) show competitive positioning. HSBC offers highest annual cap (14%) with premium features, while YF Life leads on cost efficiency. All three include 0% floor protection, but vary significantly on entry and administrative fees—critical considerations for professional investors.

Early Movers: Product Positioning in Hong Kong

Within months of the circular, Hong Kong’s top insurers moved quickly.

Sun Life Hong Kong launched its Indexed Universal Life product on May 21, 2025, positioned as first to market. The offering combines index-linked cash-value growth (with typical caps around 12% annually and a 0% floor) with flexible premiums and death benefits.[7]

HSBC Life followed in July 2025 with Aspire Prime Indexed Universal Life, differentiating on features: HSBC’s product includes a unique gold-tracking component alongside traditional equity indices, appealing to investors hedging inflation risk.[8]

YF Life Insurance International completed the early-mover cohort with its IUL launch on July 28, 2025, emphasizing fintech integration and real-time tracking for the digitally native HNWI segment.[8]

All three products target the same core market: HNWIs aged 40-65 seeking alternatives to traditional whole life, with initial minimum premiums ranging from USD 100,000 to USD 250,000 annually.[4]

Where IUL Fits in the Hong Kong HNWI Portfolio

For a Hong Kong HNWI, the choice isn’t binary: should I buy IUL or whole life? Rather, it’s architectural: how does IUL fit alongside other wealth-preservation tools?

Participating whole-life insurance still dominates Hong Kong’s HNWI segment, with good reason. These policies offer guaranteed returns plus non-guaranteed dividends from the insurer’s investment performance. They’re straightforward, carry implicit guarantees, and align with Asian cultural preferences for safety and multi-generational wealth accumulation.[9]

IUL serves a different purpose. It’s for HNWIs who:

Believe markets will outperform guaranteed-return investments over the long term

Can tolerate year-to-year volatility (even with floor protection)

Want permanent coverage with meaningful wealth accumulation beyond traditional whole life

Need death benefit liquidity to fund cross-border estate taxes across multiple jurisdictions

A typical sophisticated HNWI might structure it as:

Foundation insurance: USD 20M whole-life policy for guaranteed, predictable wealth transfer

Growth component: USD 30M IUL policy for market-linked upside and flexibility

The two serve distinct objectives within the overall estate plan.

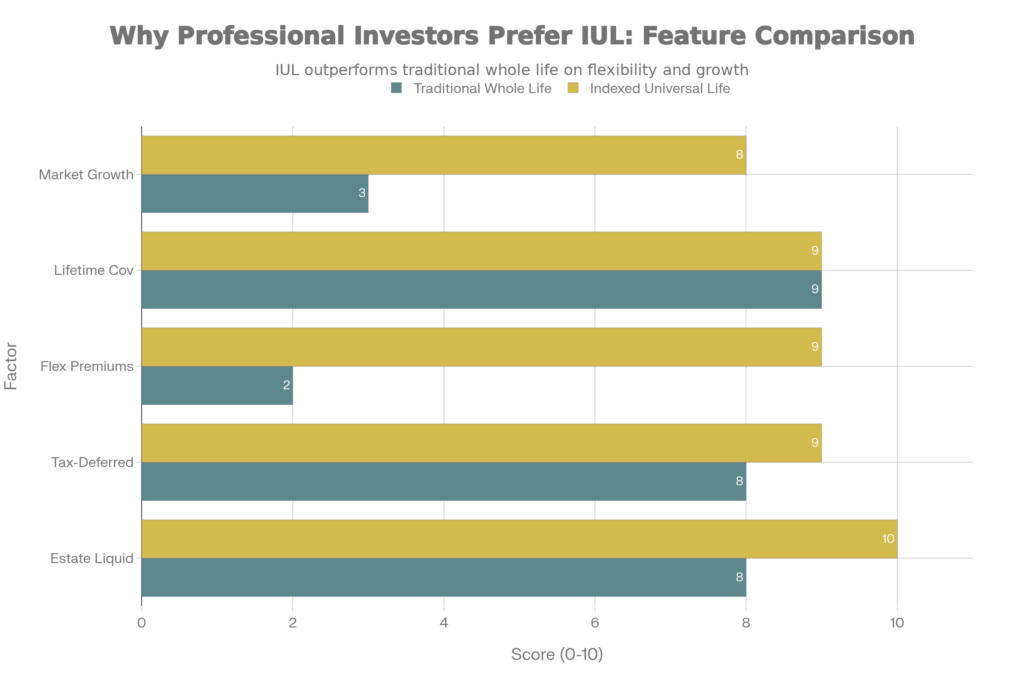

Why Professional Investor Prefer IUL

IUL’s competitive advantage lies in flexibility and growth potential. While traditional whole life excels at guarantees, IUL delivers superior market participation, flexible premiums, and estate planning benefits—critical for Hong Kong’s HNWIs navigating cross-border wealth strategies and dynamic market conditions.

Compliance and Governance: Why This Is Regulated Protection, Not Speculation

One concern advisors raise: doesn’t IUL’s market exposure make this risky for HNWIs?

The answer is no—because of how Hong Kong’s regulators structured the approval framework.

Under the March 2025 circular, IUL insurers must still:

Demonstrate suitability with professional investors (can you afford premiums? Does the product match your objectives?)

Provide detailed benefit illustrations showing realistic scenarios (not just best-case)

Disclose all fees, charges, and return assumptions transparently

Maintain product-governance processes ensuring delivery of promised benefits

This is serious regulation, not a free pass. The floor protection (typically 0%) and cap mechanism (typically 8-14% annually) constrain volatility in ways raw equity investment does not. An IUL investor isn’t exposed to a 2008-style collapse or unlimited upside; they’re in a structured wrapper.

For professional investors—people who already own stocks, real estate, private equity—this risk profile is mild. That’s precisely why regulators felt comfortable relaxing certain retail protections.[1][2]

Cross-Border Relevance: Why Timing Matters

Here’s why HNWIs in Hong Kong specifically should care about IUL’s 2025 availability.

Hong Kong attracts wealth from mainland China, Southeast Asia, the Middle East, and the UK. These globally mobile families face multi-jurisdiction tax exposure: UK property subject to inheritance tax, US business interests subject to federal estate tax, or mainland assets managed through Hong Kong structures.

Traditional whole-life insurance addresses this, but with limitations: fixed guarantees don’t flex with changing wealth levels. If an HNWI accumulates significantly more wealth post-purchase, the whole-life policy doesn’t scale to new estate-tax exposure.

IUL, with its flexible death benefit, allows mid-course adjustment. As wealth grows, the professional investor can increase policy sum assured (subject to underwriting) without complete repurchase.[5]

For families with Hong Kong as booking centre but assets spread across Singapore, Dubai, London, and New York, IUL’s permanent nature and tax-deferred growth work well. The policy functions as a portable wealth vehicle independent of any single jurisdiction’s tax rules.

Understanding the Risks: Complexity and Due Diligence

IUL isn’t for everyone, even among HNWIs. Key risks professionals should understand:

Illustration Risk: Benefit illustrations show scenarios (conservative, moderate, optimistic) but aren’t guarantees. 10-year projections depend on index performance that may not materialize.[2]

Fee Erosion: Administrative fees, mortality charges, and cost-of-insurance deductions can erode returns, especially in early policy years. Advisors should insist on transparent fee schedules.[5]

Illiquidity: It’s a permanent policy. Early surrender incurs penalties. This is a long-term commitment, not liquid investment.

Professional investors should engage independent advisors and request detailed projections, stress tests, and fee comparisons before committing. Hong Kong regulators expect this due diligence—it’s implicit in the professional-investor-only model.[1]

The Regulatory Moment: Competitive Context

March 2025’s circular represented the IA and HKMA saying: “Hong Kong can responsibly offer IUL to professional investors, and we’ve designed a framework protecting consumers while enabling innovation.”

This matters competitively. Singapore offered flexible index-linked insurance longer than Hong Kong. The US IUL market wrote USD 3.8 billion in new premiums in 2024. Hong Kong was a laggard.

The 2025 regulatory shift positions Hong Kong to compete—not by lowering protections, but by acknowledging that sophisticated investors can responsibly choose products suited to their circumstances.[2][6]

Quick Reference: IUL vs Traditional Products

Feature

Traditional Whole Life

Indexed Universal Life

Death Benefit

Fixed, guaranteed

Fixed or flexible, guaranteed

Cash Value Growth

Fixed rate (3-4% typical)

Index-linked (0% floor, 8-14% cap)

Premium Flexibility

Limited; set schedule

High; adjustable within guidelines

Fees

Lower, bundled

Higher; transparent line-item charges

Complexity

Low; straightforward

Moderate; requires index understanding

Time Horizon

20-40 years typical

30+ years (benefits from long-term growth)

Best For

Guaranteed legacy

Market-linked growth, flexible structuring

Investor Profile

Conservative, safety-focused

Professional, volatility-comfortable

Final Perspective

The March 2025 regulatory shift didn’t invent IUL in Hong Kong; insurers were developing these products. What the IA and HKMA did was provide clarity: here’s how we’ll regulate this, here’s what’s allowed, and here’s how we’ll protect professional investors without stifling innovation.

For HNWIs navigating multi-jurisdictional wealth planning, IUL is no longer theoretical. It’s available from credible carriers (Sun Life, HSBC, YF Life), with clear regulatory guardrails.

Whether it fits your circumstances depends on objectives, time horizon, and comfort with market-linked returns. That’s a conversation with a qualified advisor who understands both IUL mechanics and your global wealth picture.

But the option is now genuine. And in Hong Kong’s competitive landscape, that represents meaningful progress.

Hong Kong’s three early-mover IUL products (May-July 2025 launches) show competitive positioning. HSBC offers highest annual cap (14%) with premium features, while YF Life leads on cost efficiency. All three include 0% floor protection, but vary significantly on entry and administrative fees—critical considerations for professional investors.

IUL’s competitive advantage lies in flexibility and growth potential. While traditional whole life excels at guarantees, IUL delivers superior market participation, flexible premiums, and estate planning benefits—critical for Hong Kong’s HNWIs navigating cross-border wealth strategies and dynamic market conditions.

FAQs:

What’s the key difference between IUL and traditional whole-life insurance that makes it attractive to HNWIs?

The fundamental difference lies in growth potential and flexibility. Traditional whole-life insurance offers fixed returns (typically 3-4% annually) guaranteed by the insurer—you know exactly what your cash value will be in 10 or 20 years. This certainty appeals to conservative investors, but it also means you’re capped in terms of wealth accumulation potential. IUL, by contrast, ties your cash value to market indices (like the S&P 500 or Hang Seng). If markets perform well, your policy benefits. If markets decline, the floor protection (typically 0%) shields you from losses that year. This structure appeals to HNWIs who believe long-term markets will outperform guaranteed returns and want their insurance policy to work harder for their wealth.

Does the March 2025 regulatory change mean IUL is now available to everyone in Hong Kong, or only to wealthy investors?

The regulatory change is explicitly restricted to professional investors only. Hong Kong’s Insurance Authority (IA) did not open IUL to retail customers or the general public. Instead, they created a streamlined pathway for HNWIs and professional investors who meet specific criteria under the Securities and Futures Ordinance. A “professional investor” in Hong Kong’s context typically means: Individuals with substantial investment experience and financial resources Institutional investors (family offices, private equity firms, funds) Business owners with demonstrated investment sophistication

The regulator’s reasoning is straightforward: IUL involves index-linked returns and premium flexibility—complexity that retail customers might not fully grasp. By limiting distribution to professional investors, the IA ensures the product is sold to buyers who can genuinely evaluate its benefits and risks.

If you’re an HNWI in Hong Kong, you likely qualify. Your private-banking advisor or insurance broker can confirm whether you meet the professional-investor definition.

If I buy an IUL policy in Hong Kong as a British taxpayer with UK property and US business interests, how does the tax treatment work?

This is where Hong Kong IUL becomes strategically valuable for cross-border HNWIs. The tax treatment depends on where you’re taxed and how the policy is structured—not on where you buy the product. Generally speaking: Hong Kong: If you’re Hong Kong-domiciled, IUL policies enjoy the same tax-deferred growth as any long-term insurance product. No capital gains tax is triggered inside the policy, and death benefits paid to beneficiaries are not subject to Hong Kong estate duty (abolished in 2006). UK: If you’re UK-domiciled, the policy and its cash value are typically not subject to UK income tax during your lifetime (insurance policies enjoy preferential treatment). However, the death benefit becomes part of your estate for UK inheritance-tax purposes. With proper planning (using trusts or ILITs), this exposure can be managed.

US: If you hold US assets or are a US citizen, the IUL policy itself isn’t directly taxable to the US. However, estate-tax planning becomes more complex.

The key takeaway: Hong Kong IUL doesn’t automatically solve cross-border tax problems. But it does provide a neutral, flexible vehicle that works well alongside your overall estate-planning architecture. You must work with tax advisors in each jurisdiction (Hong Kong, UK, US, etc.) to optimize the structure.

Many HNWIs use Hong Kong IUL as an estate-tax liquidity tool—the death benefit provides cash to cover taxes in multiple jurisdictions without forcing asset sales. That strategic benefit transcends any single jurisdiction’s tax code.

What are the main risks I should understand before committing to an IUL policy?

IUL is a regulated wealth-management product, not speculation. But there are genuine risks to understand:

1. Illustration Risk Insurers provide benefit illustrations showing scenarios (conservative, moderate, optimistic). These are not guarantees. If historical market returns don’t repeat, your actual cash value may trail the “moderate” illustration. The 10-12% annual caps on IUL returns mean you won’t capture all upside in boom years.

2. Premium Obligation While IUL offers flexible premiums, you still need to pay something to keep the policy in force. If you stop paying for too long, the policy lapses. For permanent wealth-preservation goals, ongoing premium commitment is essential. This isn’t a “set and forget” product.

3. Fee Erosion Early policy years have higher cost-of-insurance charges and administrative fees. These deductions reduce the net crediting rate your cash value receives. Transparent fee schedules are essential—insist on detailed breakdowns before purchase.

4. Complexity You need to understand how index crediting works, what the caps and floors mean, and how the policy interacts with your broader wealth plan. This isn’t a product to buy without independent advice. Professional guidance is highly recommended for structuring within estate plans and multi-jurisdiction contexts.

5. Liquidity It’s permanent insurance, not liquid investment. Early surrender (withdrawing cash value before maturity) incurs penalties. If your wealth situation changes dramatically (major business sale, divorce), you may be locked into a policy structure that no longer fits.

Mitigate these risks through detailed advisor consultation, requesting stress-tested projections, and ensuring the policy aligns with your actual estate-planning objectives—not just sales pitch.

How does an IUL policy owned by a family office differ from one owned individually?

This is a critical structural distinction for ultra-high-net-worth families. Individual Ownership:

You (the HNWI) own the policy personally. The death benefit flows to your beneficiaries or estate. This works, but the policy is part of your taxable estate (albeit with planning mitigation through trusts).

Family Office / Trust Ownership: The DIFC Foundation, ADGM Trust, or other family-office vehicle owns the policy. You are the insured (the life being covered), but the family office is the policy owner. The death benefit flows to the family office, which distributes per its governing documents.

Key advantages of family-office ownership:

Institutional governance: The policy is managed as a corporate asset, not personal property. Reviews happen on a scheduled basis with independent trustees overseeing performance. Multi-generation flexibility: The family office structure allows the death benefit to benefit multiple generations, not just your immediate heirs. Estate planning becomes more fluid. Asset protection: In some jurisdictions, trusts or foundations provide stronger creditor protection than individual ownership. Administrative clarity: The family office owns multiple assets (real estate, businesses, securities, insurance policies). Having the policy sit within that structure simplifies administration and ensures consistent oversight. Succession planning: When the family office outlives the original patriarch/matriarch, the insurance policy continues as part of ongoing wealth management without friction.

For HNWIs with USD 50M+ net worth and multi-jurisdictional assets, family-office ownership is increasingly the standard approach. It aligns the insurance policy with broader family governance structures and creates institutional continuity beyond any individual’s lifetime.

If I’m a Mainland Chinese buyer purchasing an IUL policy in Hong Kong, what regulatory and practical considerations apply?

Mainland Chinese HNWIs comprise a significant portion of Hong Kong’s insurance market (28-30% of new business). Here are key considerations:

Regulatory Requirements:

You must physically be in Hong Kong to sign the policy application. Online or mainland-based applications violate IA regulations. Insurers verify your presence in Hong Kong through documentation.

Premium payments must come from legitimate sources with proper documentation. Banks and insurers increasingly scrutinize large premiums for anti-money-laundering (AML) compliance. Be prepared to provide proof of income source and wealth legitimacy.

You must meet the “professional investor” definition under Hong Kong law. Foreign investors typically qualify if they demonstrate investment experience and financial capacity.

Practical Considerations:

Remittance limits: Mainland residents face daily same-name account transfer limits (RMB 80,000) and annual foreign-exchange quotas (USD 50,000 for non-trade purposes). Larger premiums require planning: using multiple remittance methods, Hong Kong visit-based payments, or structuring through offshore accounts.

Currency diversification benefit: This is why Mainland buyers are attracted to Hong Kong IUL—policies denominated in HKD or USD provide legitimate currency diversification away from yuan exposure, particularly valuable if you’re concerned about CNY volatility or capital-control risks.

Tax reporting: While Hong Kong imposes no inheritance tax, Mainland residents must consider Chinese tax obligations. China applies worldwide income taxation for tax residents. Consult tax advisors regarding potential reporting requirements for insurance policy values and distributions.

CRS compliance: Hong Kong and mainland China both participate in the Common Reporting Standard (CRS). However, properly structured life insurance policies often fall outside CRS reporting requirements if structured correctly, providing privacy advantages while remaining fully compliant.

Strategic advantage: For Mainland families using Hong Kong as a wealth-management hub, IUL provides a sophisticated tool that’s compliant with all regulatory requirements in both jurisdictions, while offering currency diversification and cross-border wealth preservation that mainland-only insurance products cannot match.

General Counsel, Head of Compliance and Operations

Salah Mattoo is an experienced international lawyer and accomplished executive, currently serving as General Counsel and Head of Compliance. He specialises in dispute resolution, corporate and commercial transactions, regulatory compliance, and internal and external investigations across multiple jurisdictions.

Salah has acted in a range of high-profile international arbitration and cross-border litigation matters, representing corporate clients, sovereigns, and institutions in complex, high-stakes disputes. Salah's background includes advisory and leadership roles in sectors such as insurance, private equity, financial services, defence, commodities, energy, technology, and infrastructure.

In addition to his disputes practice, Salah has led the design and implementation of robust compliance programs aligned with international best practices, including AML, anti-bribery, sanctions, data privacy, ESG, and whistleblower frameworks. Salah regularly advises executive teams and boards on legal risk management, governance structures, and regulatory strategy.

With a strong track record in both contentious and transactional matters, Salah combines legal precision with strategic insight to support businesses navigating regulatory complexity and international growth. Salah is qualified in England & Wales, DIFC and ADGM. He has acted as lead counsel in international commercial courts, as well as in many international arbitrations seated in the leading arbitration centers, including Abu Dhabi, Dubai, Geneva, Hong Kong, London, New York, Paris, Riyadh, Singapore, Stockholm, Tokyo, Vienna, Washington and Zurich.

Salah holds a B.A. from University of California, Berkeley and an L.L.B and L.L.M. from The London School of Economics and Political Science (University of London).

Dubai · Geneva · Hong Kong · London · Singapore

Imran Khan

Founder & Managing Director

Imran Khan is a seasoned expert in private wealth planning and jumbo life insurance solutions, with over 10 years of experience advising ultra high net worth individuals (UHNWIs), families, and family offices across multiple jurisdictions. With a deep understanding of global wealth structuring, legacy planning, and asset protection, Imran is recognized for delivering highly customized strategies that align with clients personal, business, and multigenerational goals.

Throughout his career, Imran has worked closely with private banks, trust companies, and legal advisors to design and implement sophisticated structures involving international trusts, foundations, holding companies, and life insurance-based estate equalization plans. His expertise includes:

Life insurance for estate liquidity and succession planning

Cross-border wealth transfer and tax mitigation strategies

Pre-immigration and expatriation planning

Business continuity and key-person insurance for family enterprises

Family and corporate governance

Imran holds specialist accreditations in wealth planning and international insurance advisory and is a trusted advisor to clients across the Asia, Europe, Middle East and UK. Known for discretion, technical proficiency, and strategic insight, he has built enduring relationships with UHNW families seeking to preserve and grow their legacies in an increasingly complex regulatory environment.