The Hong Kong Wealth Surge: Leveraging Bespoke Life Insurance for a 50% Growth Market

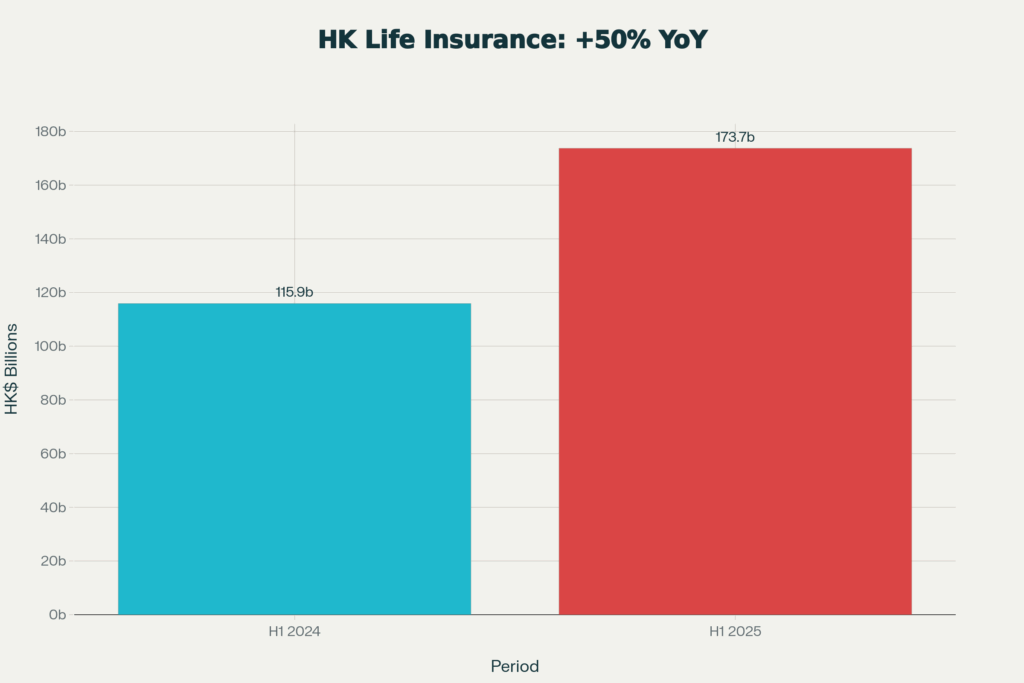

Executive Summary Hong Kong’s life insurance sector is experiencing a transformational moment. In the first half of 2025, new office premiums surged 50% year-over-year to reach HK$173.7 billion (US$22.3 billion), marking the highest first-half sales since the Insurance Authority’s establishment in 2016. This exceptional growth is driven by a confluence of factors: an explosion in […]

2nd Dec 2025 Bespoke

The Hong Kong Wealth Surge: Leveraging Bespoke Life Insurance for a 50% Growth Market

Executive Summary

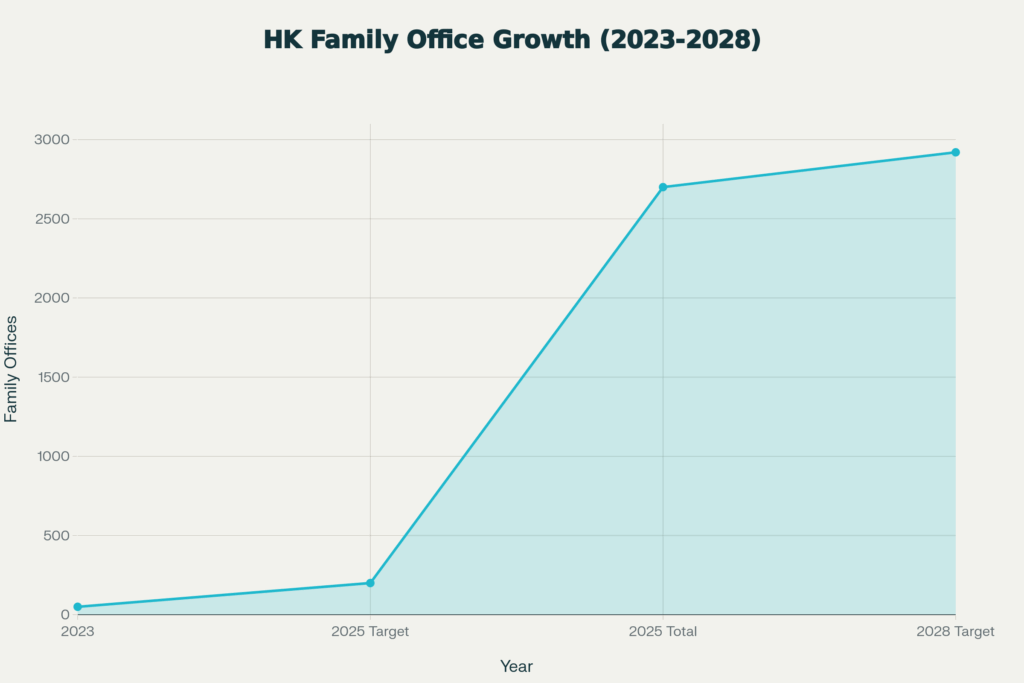

Hong Kong’s life insurance sector is experiencing a transformational moment. In the first half of 2025, new office premiums surged 50% year-over-year to reach HK$173.7 billion (US$22.3 billion), marking the highest first-half sales since the Insurance Authority’s establishment in 2016. This exceptional growth is driven by a confluence of factors: an explosion in family office establishments, surging high-net-worth individual (HNWI) demand for sophisticated wealth management solutions, and Hong Kong’s strategic positioning as Asia’s premier cross-border wealth hub. With over 2,700 family offices now operating in the city and projections indicating the insurance market will expand to US$127 billion by 2032, Hong Kong has cemented its status as the epicenter of Asia’s wealth preservation revolution.

Hong Kong’s life insurance market experienced exceptional growth with new premiums surging 50% year-over-year in the first half of 2025, reaching HK$173.7 billion

1. The Anatomy of a 50% Market Surge

1.1 Unprecedented Premium Growth Dynamics

The 50% year-over-year surge in life insurance premiums represents far more than statistical noise—it signals a fundamental restructuring of wealth management preferences among Asia’s affluent. The HK$173.7 billion recorded in H1 2025, compared to HK$115.9 billion in the same period of 2024, reflects growing recognition among HNWIs that insurance products serve as sophisticated financial instruments for wealth transfer, tax optimization, and legacy planning rather than merely protection vehicles.

Participating policies dominated this growth trajectory, accounting for HK$149.9 billion or 86.3% of new individual business premiums. These products, which combine guaranteed returns with non-guaranteed dividends based on insurer performance, appeal particularly to conservative Asian wealth holders seeking predictable wealth accumulation alongside upside potential. The popularity of participating whole-life insurance reflects a cultural preference for stability and multi-generational wealth preservation—values deeply embedded in Greater China family structures.

1.2 Demand Drivers: Beyond Traditional Protection

Three primary demand drivers underpin this exceptional growth:

First, the wealth preservation imperative has intensified amid global economic uncertainty. HNWIs from mainland China, representing 28-30% of Hong Kong policy purchases, view Hong Kong insurance as a hedge against currency volatility, particularly the yuan’s fluctuations against major currencies. Hong Kong policies denominated in HKD or USD offer multi-currency diversification that mainland products cannot match.

Second, the absence of estate duty in Hong Kong (abolished in 2006) combined with zero capital gains tax, gift tax, and inheritance tax creates a uniquely attractive environment for intergenerational wealth transfer. Life insurance death benefits bypass probate, provide immediate liquidity to beneficiaries, and remain exempt from taxation—a powerful combination for families concerned with seamless succession.

Third, regulatory evolution has expanded product sophistication. The March 2025 joint circular from the Insurance Authority and Hong Kong Monetary Authority clarifying the framework for Indexed Universal Life (IUL) products opened new avenues for HNWIs seeking market-linked growth with downside protection. This regulatory modernization signals Hong Kong’s commitment to remaining at the forefront of insurance innovation.

Hong Kong’s family office ecosystem has grown exponentially from 50 offices in 2023 to over 2,700 in 2025, with the government targeting an additional 220 offices by 2028

2. The Family Office Catalyst: Fueling Demand for Wealth Management Solutions

2.1 Exponential Growth in Family Office Establishments

Hong Kong’s family office ecosystem has undergone explosive growth, expanding from approximately 50 offices when tax concession policies launched in 2023 to over 2,700 by September 2025. This represents not merely quantitative expansion but a qualitative transformation in how ultra-high-net-worth families approach wealth governance.

The government’s achievement of its initial target—attracting 200 family offices by end-2025—occurred nine months ahead of schedule. InvestHK has now launched “Family Office 2.0,” targeting an additional 220 family offices by 2028, with expanded focus on European, Middle Eastern, and broader Asian markets beyond mainland China. This strategic internationalization reflects Hong Kong’s ambition to rival Singapore as the region’s pre-eminent family office destination.

2.2 Tax Concessions: The Structural Advantage

The legislative foundation supporting this growth rests on compelling tax incentives. Single Family Offices (SFOs) managing Family-owned Investment Holding Vehicles (FIHVs) with minimum assets of HK$240 million (US$31 million) qualify for 0% profits tax on qualifying transactions. These concessions, effective from the 2022/23 year of assessment, apply to diverse asset classes including equities, debt securities, foreign exchange, commodities, and—following 2025 enhancements—emission derivatives, insurance-linked securities, private credit, and digital assets.

Hong Kong’s territorial tax system amplifies these advantages. No capital gains tax, no withholding tax on dividends and interest, and no VAT or sales tax create a frictionless environment for wealth accumulation. For families with cross-border structures, Hong Kong-based family offices can incorporate vehicles in any jurisdiction while operating from Hong Kong, providing unparalleled flexibility.

2.3 Family Offices as Insurance Demand Multipliers

Family offices function as institutional buyers of sophisticated insurance solutions, fundamentally altering the demand landscape. Unlike individual purchasers, family offices approach insurance strategically, integrating policies into holistic wealth architectures that span generations and jurisdictions.

Research indicates that family offices increasingly view insurance as necessary rather than optional within comprehensive wealth planning. Products must address multiple generations simultaneously, provide cross-jurisdictional coverage, and incorporate tax optimization features. This drives demand for Private Placement Life Insurance (PPLI), which allows families to house both bankable and non-bankable assets (private equity, real estate, art, digital assets) within tax-efficient insurance wrappers.

The presence of 2,700+ family offices managing combined assets exceeding US$100 billion creates substantial, sustained demand for high-premium policies. Major insurers report that jumbo policies—those with sums assured exceeding US$10 million—have become increasingly common, reflecting the concentration of wealth and sophistication of planning requirements.

3. Bespoke Insurance Solutions: Tailored Wealth Transfer for Asian HNWIs

3.1 The Product Spectrum: From Participating Policies to PPLI

Asian HNWIs now access a sophisticated spectrum of insurance products, each addressing specific wealth management objectives:

Participating Whole Life Insurance remains foundational, offering guaranteed protection combined with dividend potential. Insurers invest premiums in diversified portfolios (typically 50-90% in bonds and fixed income, with equity and alternative allocations). Policyholders receive both guaranteed cash values and non-guaranteed dividends that can accumulate with interest or be withdrawn, providing flexibility for changing family needs.

Private Placement Life Insurance (PPLI) represents the apex of bespoke solutions for ultra-high-net-worth families. PPLI functions as a private placement because underlying assets are bespoke, not merely bankable securities. These policies can house operating businesses, real estate, private equity, luxury assets, and digital holdings within a compliant insurance structure. The insurer becomes the legal owner, providing privacy from Common Reporting Standard (CRS) disclosure while allowing policyholders to maintain investment discretion through qualified portfolio managers.

PPLI’s appeal centers on five key advantages: Privacy protection through compliant structures; Asset protection by law from creditors and bankruptcy; Tax savings through deferral and estate planning; Estate liquidity ensuring sufficient cash at death; and Simplified reporting as the insurer reports rather than the policyholder. For families with complex, multi-jurisdictional holdings, PPLI can consolidate entire portfolios under one structure while preserving existing banking and investment relationships—the assets remain with trusted advisors, merely with new legal ownership.

Indexed Universal Life (IUL) insurance, newly available to professional investors following March 2025 regulatory clarification, combines permanent life coverage with cash value linked to financial index performance. IUL offers market participation with downside protection through guaranteed floors, appealing to growth-oriented HNWIs who want equity exposure without full downside risk. The tax-deferred accumulation within IUL policies, combined with flexible premium payments and death benefits, positions these products as alternatives to traditional investment portfolios for wealthy, mobile families.

3.2 Wealth Transfer Mechanics: Insurance Advantages

Life insurance provides structural advantages over alternative wealth transfer mechanisms that resonate particularly strongly with Asian families:

Immediate Liquidity: Unlike estates that may require months or years to settle, life insurance death benefits provide immediate cash to beneficiaries. This liquidity prevents forced liquidation of family businesses or real estate during succession, preserving core asset value.

Probate Bypass: Insurance proceeds paid to named beneficiaries avoid probate entirely, ensuring privacy and reducing estate settlement costs. For families concerned about confidentiality—a paramount consideration in Asia—this characteristic proves invaluable.

Creditor Protection: In many common-law jurisdictions, properly structured life insurance policies enjoy protection from creditors. When combined with irrevocable beneficiary designations, these protections strengthen significantly, safeguarding family wealth from business risks or litigation.

Beneficiary Certainty: Direct beneficiary designations in insurance policies prevent inheritance disputes by creating clear, legally enforceable distribution instructions. Surveys indicate 67% of Greater China HNWIs value beneficiary designations specifically to avoid family conflicts during wealth transfer.

Tax Efficiency: The combination of tax-deferred accumulation during the policyholder’s lifetime and tax-free death benefits creates unmatched efficiency. In Hong Kong’s zero-estate-duty environment, wealthy families can transfer substantial sums without any inheritance taxation—a capability that distinguishes the city from most developed markets.

4. China Considerations and Cross-Border Wealth Strategies

4.1 The Mainland China Factor: 30% of Market Demand

Mainland Chinese buyers constitute approximately 28-30% of Hong Kong’s life insurance sales, a proportion that has remained remarkably stable even as absolute volumes surge. This sustained demand reflects structural advantages Hong Kong policies offer mainland residents beyond mere financial returns.

Currency Diversification: With the yuan subject to periodic volatility and capital controls limiting outbound investment, Hong Kong life insurance policies denominated in HKD or USD provide mainland families with legitimate currency diversification. Whole life policies with USD components function as long-term stores of value in hard currency, insulated from domestic monetary policy shifts.

Superior Product Features: Mainland HNWIs cite several reasons for preferring Hong Kong insurance: better coverage breadth, lower premiums for equivalent protection, higher returns on savings-linked products, more flexible policy terms, and broader exclusion exemptions. International insurers’ Hong Kong operations also carry perceived credit quality advantages given their global capitalization and regulatory oversight.

Wealth Transfer Clarity: Hong Kong’s common-law framework provides clearer beneficiary rights and more predictable policy treatment upon death compared to mainland China’s evolving civil-law trust and inheritance systems. For families concerned about multi-generational wealth preservation, this legal certainty justifies premium costs.

Sophisticated mainland families increasingly employ integrated cross-border structures combining Hong Kong insurance with onshore holdings:

Greater Bay Area Integration: The Cross-boundary Wealth Management Connect scheme, launched in 2021, allows GBA residents to invest up to RMB 3 million in cross-border wealth products. While insurance products aren’t yet fully integrated into Wealth Management Connect, the Insurance Authority and mainland regulators are developing an “Insurance Connect” framework that would enable after-sales service centers in GBA cities and potentially cross-border policy sales.

Remittance Strategies: Mainland residents purchasing Hong Kong policies must navigate remittance limits. The RMB 80,000 daily same-name account transfer limit requires planning for larger premium payments. Families typically structure purchases through multiple methods: direct premium payments during Hong Kong visits, offshore account funding, or utilizing the USD 50,000 annual foreign exchange quota for non-trade purposes.

Trust and Corporate Structures: Leading-edge planning combines Hong Kong insurance policies with offshore trusts and family office structures. A typical architecture might involve:

(1) A Hong Kong or offshore trust as policy owner;

(2) PPLI or participating whole-life policies held within the trust;

(3) A Hong Kong family office managing the trust and coordinating with mainland business interests;

(4) Beneficiary structures spanning multiple generations and jurisdictions.

This layered approach addresses China-specific concerns including future estate duty risk (currently absent but under periodic consideration), divorce protection (critical given complex family structures), and creditor shielding for entrepreneurs with business exposures.

Purchase Requirements: Mainland residents must physically be in Hong Kong when applying for policies and signing documents—online or mainland-based applications violate regulations. Insurance Authority rules mandate that insurers verify purchaser presence in Hong Kong through documentation.

Premium Payment: Premiums must be paid from legitimate sources with proper documentation. Banks and insurers increasingly scrutinize large premium payments to ensure anti-money-laundering compliance, requiring proof of income sources and wealth legitimacy.

Tax Reporting: While Hong Kong imposes no inheritance tax, mainland residents must consider Chinese tax obligations. China applies worldwide income taxation for tax residents, and families should consult advisors regarding potential reporting requirements for insurance policy values and distributions.

Common Reporting Standard (CRS): Hong Kong and mainland China both participate in CRS, requiring financial institutions to report certain account information to tax authorities. However, properly structured life insurance policies often fall outside CRS reporting requirements if structured correctly, providing privacy advantages while remaining fully compliant.

5. Market Outlook and Strategic Implications

5.1 Growth Trajectory Through 2032

Hong Kong’s insurance market faces extraordinarily favorable structural conditions supporting sustained expansion. Fortune Business Insights projects the total market will grow from US$80.38 billion in 2025 to US$127.02 billion by 2032, representing a 6.8% compound annual growth rate—significantly above global insurance market averages.

Multiple catalysts support this projection:

Demographic Tailwinds: Hong Kong’s elderly population (65+) is projected to expand from 1.45 million in 2021 to 2.74 million by 2046, driving demand for retirement and healthcare solutions. Simultaneously, Asia’s HNWI population continues growing rapidly, with the region expected to see US$9.7 trillion in additional wealth by 2028.

Intergenerational Wealth Transfer: An estimated US$5.8 trillion will transfer between generations in Asia-Pacific by 2030, with much of this wealth currently concentrated in founder-generation hands. As McKinsey research indicates, 91% of Asian family business founders want to maintain family leadership, yet 28% report heirs lack interest and 24% say successors are unprepared. This succession crisis creates enormous demand for insurance-based solutions providing both liquidity and structured transfer mechanisms.

Product Innovation: The introduction of IUL products for professional investors, ongoing PPLI adoption, and development of hybrid solutions combining insurance with trust and corporate structures will expand the addressable market. Insurers increasingly develop bespoke underwriting capabilities for jumbo policies, enabling customization at the UHNW segment.

Cross-Border Facilitation: As Insurance Connect and other GBA integration initiatives mature, cross-border insurance purchasing will become more seamless. Mainland demand should remain robust given structural advantages Hong Kong policies provide.

5.2 Competitive Landscape Evolution

The market’s explosive growth has intensified competition among insurers and wealth management institutions. HSBC Life maintained market leadership with 21.5% market share in Q1 2025, writing over HK$20 billion in new premiums. However, challengers including AIA, Prudential, Manulife, FWD, and Sun Life are investing heavily in HNWI-focused distribution and product development.

Success in this market requires:

Private Banking Integration: Leading insurers have embedded specialists within private banks, enabling seamless integration of insurance into holistic wealth planning conversations. This embedded model ensures insurance recommendations align with broader family office objectives.

Jurisdictional Expertise: Advisors must understand multi-jurisdictional tax and estate planning implications. The most valued professionals can structure solutions spanning Hong Kong, mainland China, Singapore, and Western jurisdictions simultaneously.

Bespoke Underwriting: Standard policies cannot address UHNW needs. Insurers developing case-by-case underwriting capabilities for large, complex situations gain competitive advantages. This includes flexibility on policy structures, premium financing options, and customized beneficiary arrangements.

Ecosystem Partnerships: Insurance solutions rarely stand alone at the UHNW level. Partnerships with trust companies, tax advisors, legal specialists, and family office consultants create comprehensive service capabilities that families require.

5.3 Policy and Regulatory Outlook

Hong Kong’s government views the insurance and family office sectors as strategic growth pillars. The 2025-26 Budget announced further enhancements to family office tax concessions, expanding qualifying transactions to include insurance-linked securities, digital assets, and private credit. Legislative proposals targeting 2026 implementation will increase flexibility and attractiveness for global families.

The Insurance Authority continues modernizing regulatory frameworks, balancing innovation encouragement with consumer protection. The IUL circular demonstrates this approach—enabling product development for sophisticated investors while maintaining guardrails. Future regulatory developments may include:

Expanded Insurance Connect enabling after-sales services in GBA cities

Further clarification on PPLI structures and permissible assets

Enhanced disclosure requirements for complex products

Streamlined processes for HNWI policy approvals

These regulatory directions suggest sustained government commitment to maintaining Hong Kong’s competitive edge in wealth management and insurance.

6. Strategic Recommendations for Wealth Holders

For HNWIs and UHNWIs considering Hong Kong insurance as part of wealth strategies, several recommendations emerge:

Early Planning: Estate and succession planning should begin decades before anticipated wealth transfer. Insurance policies require time to accumulate value and demonstrate premium payment patterns supporting legitimate planning rather than death-bed restructuring.

Integrated Architecture: Avoid viewing insurance in isolation. Optimal structures combine policies with trusts, family offices, and corporate vehicles, each component serving specific functions within the overall wealth architecture.

Professional Guidance: The sophistication of modern wealth structures demands expert advisors. Families should assemble teams including insurance specialists, tax advisors familiar with both Hong Kong and home jurisdiction rules, estate planning attorneys, and experienced trustees.

Product Diversification: Different products serve different objectives. A comprehensive insurance program might include participating whole life for guaranteed legacy preservation, PPLI for tax-efficient asset aggregation, IUL for growth-oriented components, and term insurance for pure protection needs.

Regular Reviews: Tax laws, family circumstances, and financial markets evolve. Annual reviews ensure structures remain optimal and compliant, adjusting for regulatory changes, family events (births, marriages, divorces), and wealth accumulation or distribution.

Privacy and Compliance Balance: While privacy is valuable, all structures must comply fully with applicable regulations. Aggressive tax avoidance schemes or non-compliant offshore structures risk substantial penalties and reputational damage.

Final Words

Hong Kong’s 50% surge in life insurance premiums during H1 2025 represents far more than a statistical anomaly—it signals the maturation of Asia’s wealth management ecosystem and Hong Kong’s ascendance as the region’s premier hub for sophisticated, cross-border wealth preservation. The convergence of family office proliferation (2,700+ and growing), favorable tax policies (zero estate duty and family office concessions), product innovation (IUL, PPLI, participating policies), and structural advantages (common law certainty, currency flexibility, regulatory sophistication) creates a self-reinforcing growth dynamic.

For the estimated US$5.8 trillion in wealth transferring between Asian generations by 2030, bespoke insurance solutions provide unmatched combinations of tax efficiency, liquidity provision, privacy protection, and multi-generational flexibility. As mainland Chinese families increasingly utilize Hong Kong structures for cross-border wealth management, and as global UHNW families recognize Hong Kong’s competitive advantages, the city’s insurance market appears poised for sustained expansion toward the projected US$127 billion market size by 2032.

The wealth holders who will benefit most from this environment are those who act strategically now—engaging expert advisors, constructing integrated multi-jurisdictional structures, and leveraging the full spectrum of available insurance instruments. In an era of global tax transparency, regulatory complexity, and family succession challenges, Hong Kong’s insurance and family office ecosystem offers Asian HNWIs a rare combination: world-class sophistication with uniquely favorable structural conditions. The 50% growth rate may moderate, but the underlying drivers ensuring Hong Kong’s central role in Asia’s wealth preservation revolution remain robust and accelerating.

General Counsel, Head of Compliance and Operations

Salah Mattoo is an experienced international lawyer and accomplished executive, currently serving as General Counsel and Head of Compliance. He specialises in dispute resolution, corporate and commercial transactions, regulatory compliance, and internal and external investigations across multiple jurisdictions.

Salah has acted in a range of high-profile international arbitration and cross-border litigation matters, representing corporate clients, sovereigns, and institutions in complex, high-stakes disputes. Salah's background includes advisory and leadership roles in sectors such as insurance, private equity, financial services, defence, commodities, energy, technology, and infrastructure.

In addition to his disputes practice, Salah has led the design and implementation of robust compliance programs aligned with international best practices, including AML, anti-bribery, sanctions, data privacy, ESG, and whistleblower frameworks. Salah regularly advises executive teams and boards on legal risk management, governance structures, and regulatory strategy.

With a strong track record in both contentious and transactional matters, Salah combines legal precision with strategic insight to support businesses navigating regulatory complexity and international growth. Salah is qualified in England & Wales, DIFC and ADGM. He has acted as lead counsel in international commercial courts, as well as in many international arbitrations seated in the leading arbitration centers, including Abu Dhabi, Dubai, Geneva, Hong Kong, London, New York, Paris, Riyadh, Singapore, Stockholm, Tokyo, Vienna, Washington and Zurich.

Salah holds a B.A. from University of California, Berkeley and an L.L.B and L.L.M. from The London School of Economics and Political Science (University of London).

Dubai · Geneva · Hong Kong · London · Singapore

Imran Khan

Founder & Managing Director

Imran Khan is a seasoned expert in private wealth planning and jumbo life insurance solutions, with over 10 years of experience advising ultra high net worth individuals (UHNWIs), families, and family offices across multiple jurisdictions. With a deep understanding of global wealth structuring, legacy planning, and asset protection, Imran is recognized for delivering highly customized strategies that align with clients personal, business, and multigenerational goals.

Throughout his career, Imran has worked closely with private banks, trust companies, and legal advisors to design and implement sophisticated structures involving international trusts, foundations, holding companies, and life insurance-based estate equalization plans. His expertise includes:

Life insurance for estate liquidity and succession planning

Cross-border wealth transfer and tax mitigation strategies

Pre-immigration and expatriation planning

Business continuity and key-person insurance for family enterprises

Family and corporate governance

Imran holds specialist accreditations in wealth planning and international insurance advisory and is a trusted advisor to clients across the Asia, Europe, Middle East and UK. Known for discretion, technical proficiency, and strategic insight, he has built enduring relationships with UHNW families seeking to preserve and grow their legacies in an increasingly complex regulatory environment.

{kind=link}